22/11/2021

Craft Spirits Outpace Growth of Non-Craft Spirits in the US

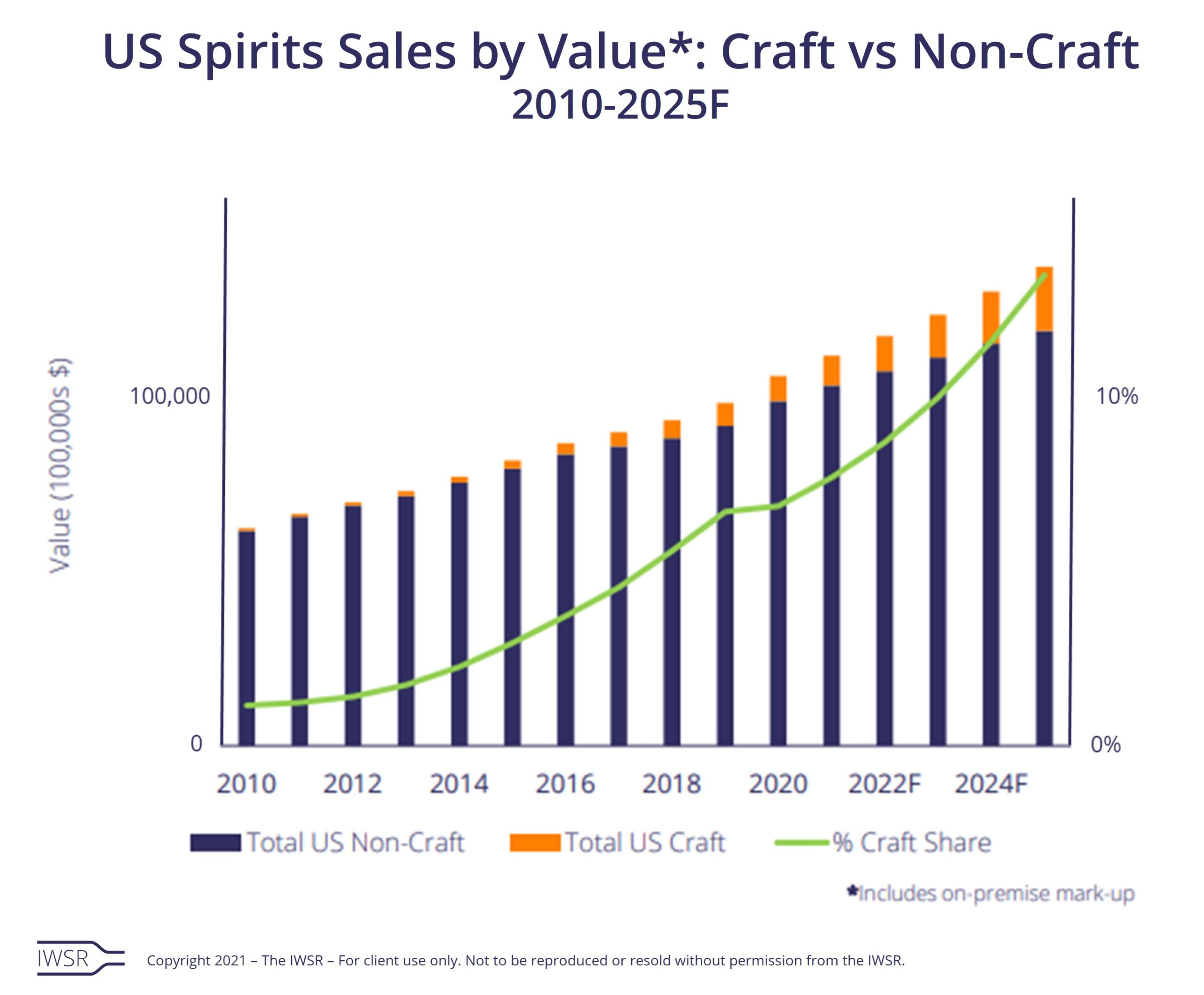

Craft spirits achieve 7% value share of total US spirits market; share of market is expected to almost double by 2025

Craft brands may make up a relatively small percentage of the total spirits industry in the US, but the fast-growing segment is set to vastly outperform the mainstream market in the coming years, according to IWSR data.

Despite the turmoil caused by the coronavirus pandemic, in 2020, craft spirits in the US registered a volume gain of close to +8%, while non-craft spirits volumes posted approximately +5% growth. This allowed the craft segment to achieve a 5% volume share of the total US spirits market, and a 7% value share.

The growth gap between mainstream and craft spirits is set to widen in the coming years, with IWSR predicting a +21% CAGR in US craft spirits for 2020-25, while US non-craft spirits is expected to register a +4% CAGR for the same period. This demonstrates that the trend for premium, artisanal spirits is gaining significant traction stateside.

While the craft segment is clearly buoyant, growth over the next five years will decelerate compared to the previous five years, due to increasing market maturity and competition.

Riding out the storm of the pandemic

Craft distilleries faced numerous challenges throughout the pandemic – including forced closures of tasting rooms and a lack of access to bars and restaurants, both key revenue drivers for smaller producers – but the impact on sales was less severe than expected.

Lockdown measures forced distillers to diversify their sales channels – a move aided by the loosening of alcohol legislation – by pivoting to ecommerce and direct-to-consumer, and investing in growing their outdoor entertainment spaces. Brands also more aggressively sought to expand distribution and implemented successful social media campaigns that enhanced their connection with local communities. These are strategic changes that will continue to pay dividends in the longer term.

“While there was a substantial deceleration in growth, craft producers and indeed the total US beverage alcohol market as a whole, performed better than projected last year due to consumption switching to the home-premise,” says IWSR analyst Ryan Lee.

In fact, while there was a record 56 distillery closures in the US in 2020, the craft segment saw the opening of 33 more distilleries than in 2019. While this represents a significant deceleration of new openings compared to previous years, it is a testament to the buoyancy of the sector in a time of heightened turmoil. The number of new craft distilleries is set to significantly ramp up in the next four years, with a predicted 265 set to open in 2025 alone.

Craft spirits steal market share

In both value and volume terms, the craft spirits sector is projected to continue to take share of total spirits, with craft’s value share reaching the double-digit milestone in 2024, at 12%.

Back in 2015, craft’s volume market share was just 2%; by 2020, this had more than doubled to almost 5%. An even greater gain was seen in value terms, with 2015’s share of 3% increasing to 7% by 2020.

“The craft category has benefited from premiumisation as higher average prices help US consumers become accustomed to premium-plus offerings,” says Lee.

By 2025, craft spirits are forecasted to increase their volume market share to nearly 10%, and over 13% in market share value. Driving this will be brands’ national distribution expansion, some of which will be the result of acquisitions by larger groups.

Dominant craft categories

All craft spirits categories are predicted to post growth in the years to 2025. Even categories that are seeing declines in the total market are forecasted to post positive gains in craft. Rum is a prime example – the total US rum category is expected to see a 2020-2025 CAGR volume decline of -1%, while craft rum is forecasted to grow +12% in the five-year period.

The biggest category in US craft spirits is US whiskey, which has a 36% share. Sub-categories such as Tennessee and blended whiskey are expected to hold the greatest volume growth potential within total US whiskey. However, craft gin is forecasted to post the greatest growth in total spirits over the forecast period. In 2020, craft gin only possessed a 9% share of the total US craft spirits market, but the category is forecasted to register a CAGR of +23% from 2020 to 2025. This compares to a +2% CAGR for total gin in the US over the same period.

Craft gin benefits from a significant price premium: while the average retail price of a 750ml bottle of gin sold in the US last year was US$16.77, the average craft gin retails for more than US$30. “Brands are also driving up their popularity with consumers by leveraging regional botanicals, aged expressions, flavours and other innovations,” says Lee.

Other categories that are emerging within the craft spirits space in the US and carving out their own niche following are flavoured whiskey and agave-based spirits. While innovation continues to drive the evolution of the flavoured whiskey space, there is an opportunity for agave spirits to fill the growing gap left by Tequila, which continues to face substantial supply challenges.

“These findings suggest the US craft spirits segment has ample opportunities for evolution and growth, and continues to be an attractive investment proposition for brands,” says Lee.

You may also be interested in reading:

Brewers turn to product diversification to secure long-term growth in the US

Vodka’s premiumisation challenges and convergence with hard seltzers

Hard seltzers are evolving, not dying

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All, Spirits | MARKET: All, North America | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies