26/10/2023

Does tequila’s growth mirror that of the gin boom?

IWSR analysis outlines five major differences in the growth drivers for tequila versus gin – which should equip tequila to grow faster, and for longer, in the years ahead

Gin and tequila are two major success stories of the global spirits market – but tequila is now outstripping gin in growth terms, primarily due to a combination of product variety, price mix and diversity of occasions.

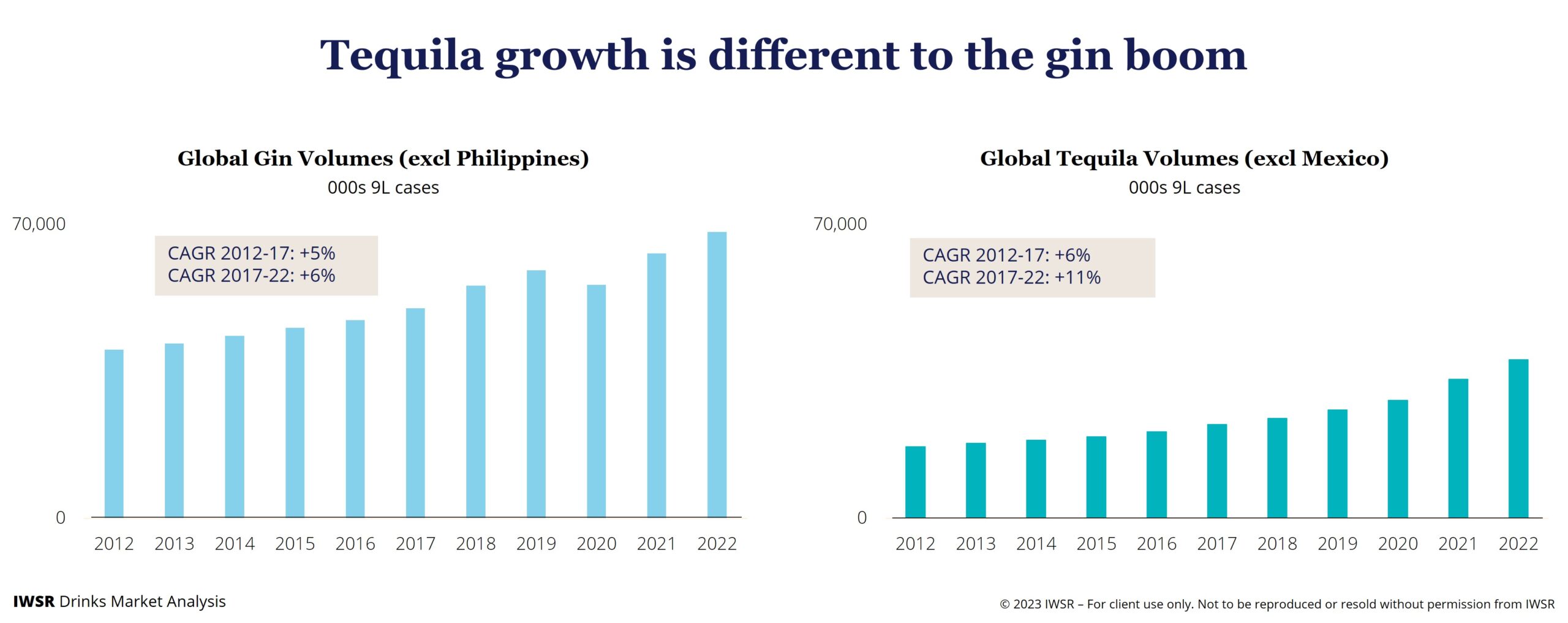

Both categories have performed strongly over the past decade: global gin volumes (excluding the large, low-priced Philippines market) grew at a CAGR of +5% between 2012 and 2017, and +6% between 2017 and 2022, according to IWSR figures.

Tequila’s performance has been even more impressive, with global volumes (excluding the large home market of Mexico) rising at a CAGR of +6% between 2012 and 2017, accelerating to +11% between 2017 and 2022.

Meanwhile, IWSR forecasts show much brighter fortunes for tequila in the years ahead: while gin volumes (excluding the Philippines) are expected to grow at a CAGR of +3% between 2022 and 2027, tequila (excluding Mexico) is forecast to expand at a volume CAGR of +9% over the same timescale.

These contrasting expectations are underscored by five major differences in the attributes of the two categories – which should equip tequila to grow faster, and for longer, in the years ahead.

1- Market mix

Gin’s growth is more geographically diverse, building on the historic base of a large, well-established category. Growth persists in a number of countries, but the gin boom in the key markets of the UK and Spain has now run its course.

Meanwhile, tequila remains hugely reliant on the US market, which accounts for over 60% of global volumes, according to IWSR figures.

However, agave spirits are currently experiencing dynamic growth in a number of countries around the world, with 15 of the 20 largest agave spirits markets experiencing volume growth of more than 20% in 2022, according to IWSR numbers – including the UK, Spain, Australia, Japan and Canada.

Of the 20 largest markets, 14 are expected to see agave spirits volumes grow at a CAGR of above +5% between 2022 and 2027.

Nonetheless, the US remains the number one priority for most brand owners, with other markets being allotted small allocations of key tequila brands as a result – and IWSR expects this dynamic to continue.

“Tequila producers are likely going to continue to invest most of their time in the US market, where they can more easily sell their products with better margins, compared to other countries,” notes José Luis Hermoso, IWSR research director, Central and South America.

“There is definitely demand for tequila in other markets that has not been satisfied, but the category needs to be built in many other countries that have the potential, but not yet the consumer interest and knowledge, for tequila to move forward; this will probably not happen until a slowdown in US demand is confirmed.”

2- Product type

Gin’s continuing growth has largely been predicated on innovation to revive what had become a rather jaded category – including the catalyst of the craft gin movement and diversity to maintain consumer interest: flavours, esoteric botanicals, local/craft products.

However, the vast majority of gins on the market are unaged spirits that have to rely on cues such as packaging and ingredients to persuade consumers to trade up to a more expensive product.

By contrast, tequila has greater inherent diversity, with a ladder of different age categories (blanco, reposado, añejo, extra añejo), and is less dependent on flavour innovation or the craft spirits segment for success.

3- Price range

In turn, these differences in product type impact the pricing range of the two categories, with tequila spanning a much broader range than gin, and much of the growth in the dominant US market up to now coming at super premium and premium-and-above price points.

“Tequila is much more present than gin at the very high end (prestige and prestige-plus, status spirits), simply because its liquid and ageing classification justify, in some cases, very high pricing – and this is accepted by consumers,” says Hermoso.

“However, gin – which is usually non-aged – has relatively less to offer in order to be accepted as a prestige spirit with similar status to Cognac, single malt or high-end tequila.”

4- Consumption occasions

Gin’s continued growth in many markets around the world has largely been built on the popularity of the aperitivo/early evening occasion, where it plays into consumer preferences for lighter, more refreshing drinks with lower ABVs.

Tequila, meanwhile, has reinvented itself in recent years, moving from its historic positioning as a late-night, high-energy option to a more diverse mix involving sophisticated cocktails and high-end sipping and savouring.

“The fact that tequila can be consumed neat or mixed, depending on the occasion, consumer and quality of the liquid, is an advantage,” says Hermoso. “Even the brands that initiated the gin revival 20 years ago are consumed mixed, as are flavoured gins, and little or no gin is sipped or consumed on the rocks as most very high-end spirits are. This also tends to justify the higher price points tequila is able to command.”

5- Provenance and authenticity

While gin is able to promote provenance/authenticity cues – using the credentials of a local craft distillery, or locally sourced botanicals – the fact remains that gin can be made anywhere on the planet, while tequila production is confined to a legally restricted geographical area.

“If it is easier for tequila to play the luxury card, the same is also true for provenance and authenticity,” says Hermoso. “Tequila has to be produced in Mexico, whereas gin can be made anywhere. I think there is no doubt that provenance and authenticity are important factors for consumers in many markets today.”

Planning go-to-market strategies

Learning from gin’s growth curve, tequila brand owners should keep a close eye on nascent tequila markets outside of the US and Mexico.

With restrictions on tequila sourcing, other agave and agave-adjacent categories, such as sotol and bacanora, could provide opportunities that build on tequila’s momentum as well.

Some producers are already planting agave plants locally. In India, for example, Maya Pistola Agavepura is produced from 100% Wild Agave Americana, sourced from the Deccan Plateau of India, and produced in Goa. Launched in 2017, Desert Door Original Texas Sotol is distilled from wild-harvested sotol, a plant that is a cousin of agave and grows in West Texas and Mexico. Black Snake Distillery in Australia produces a range of agave spirits made with locally grown agave and inspired by Mexican traditions.

For gin, producers will need to communicate clear points of differentiation to stand out in a crowded market, and some gin brand owners may look to portfolio rationalisation in order to prioritise investment decisions.

You may also be interested in reading:

Home consumption vs the on-trade: have pandemic behaviours become entrenched?

Consumer confidence in the US remains broadly positive

The 8 drivers of change for beverage alcohol in 2023 and beyond

The above analysis reflects IWSR data from the 2023 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All, Spirits | MARKET: All | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies