27/04/2023

Key statistics: the no-alcohol and low-alcohol market

IWSR analyses the growth drivers for the no/low-alcohol market

The No- and Low-Alcohol Market:

Category performance and growth drivers

- No-alcohol products spearhead overall category growth

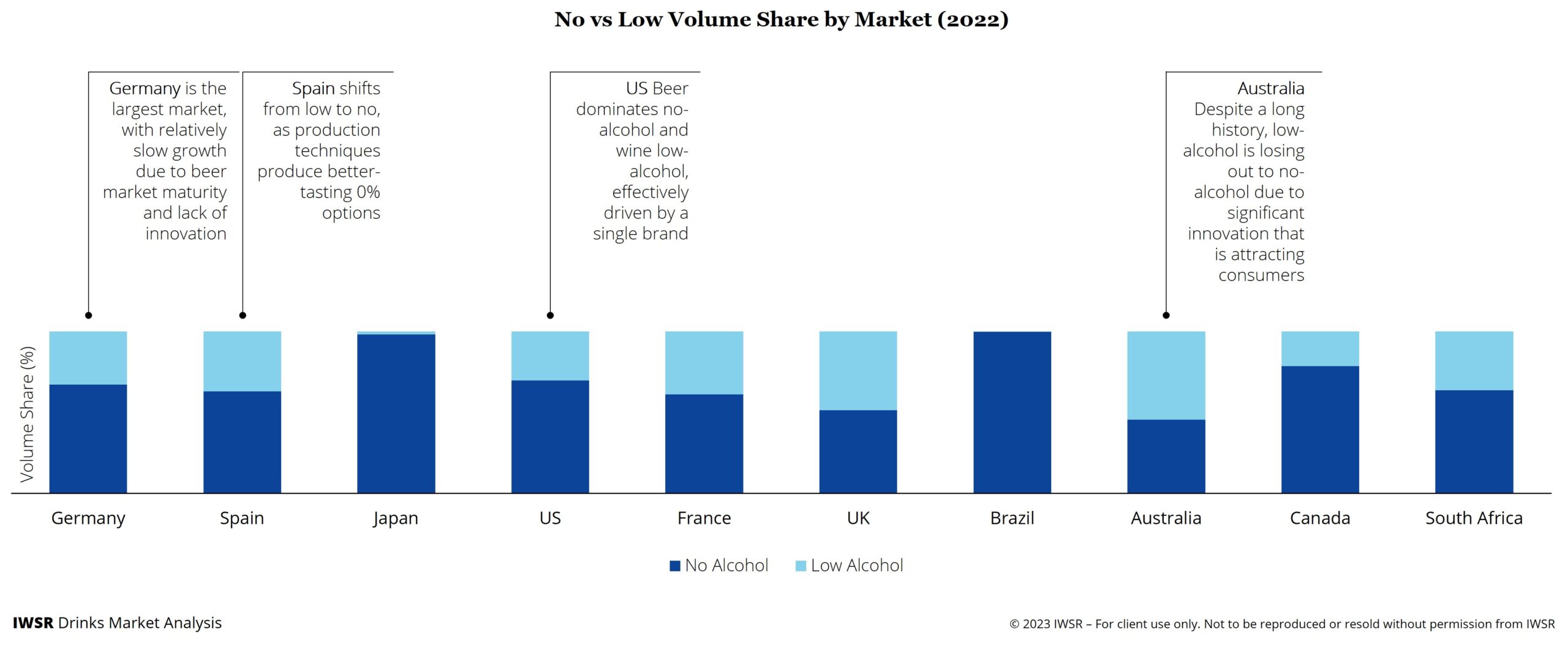

- No-alcohol volumes grew 9% in 2022, increasing their share of the overall no/low-alcohol space in the world’s 10 leading no/low markets to 70%, up from 65% in 2018.

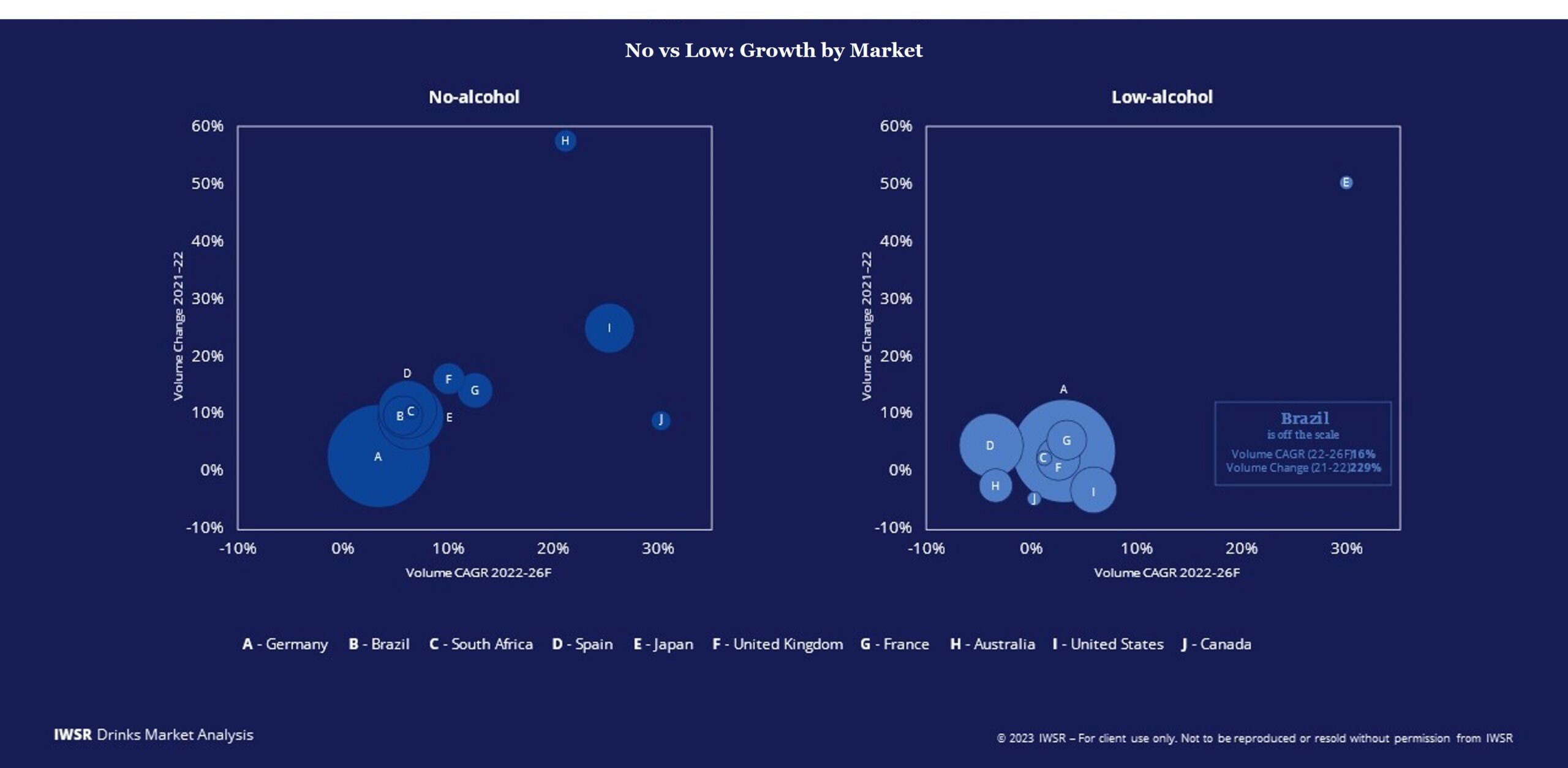

- The majority (41%) of no/low consumers choose no/low options on certain occasions, and full-strength on others. This behaviour is driving no- over low-alcohol growth across many key markets. Pair this with the rise of functionality, much of which is restricted to no-alcohol by regulations, and the result is a strong performance from no-alcohol overall. The countries where low-alcohol is leading growth rates, such as Japan and Brazil, are early-stage low-alcohol markets with a small volume base.

- The pace of growth of the no/low-alcohol category is expected to surpass that of the last 4 years, with forecast volume CAGR of +7%, 2022-26, compared to +5%, 2018-22. No-alcohol will spearhead this growth, expected to account for over 90% of the forecast total category volume growth. IWSR expects no-alcohol volumes to grow at a compound annual growth rate (CAGR) of +9% between 2022 and 2026.

Who is driving this growth?

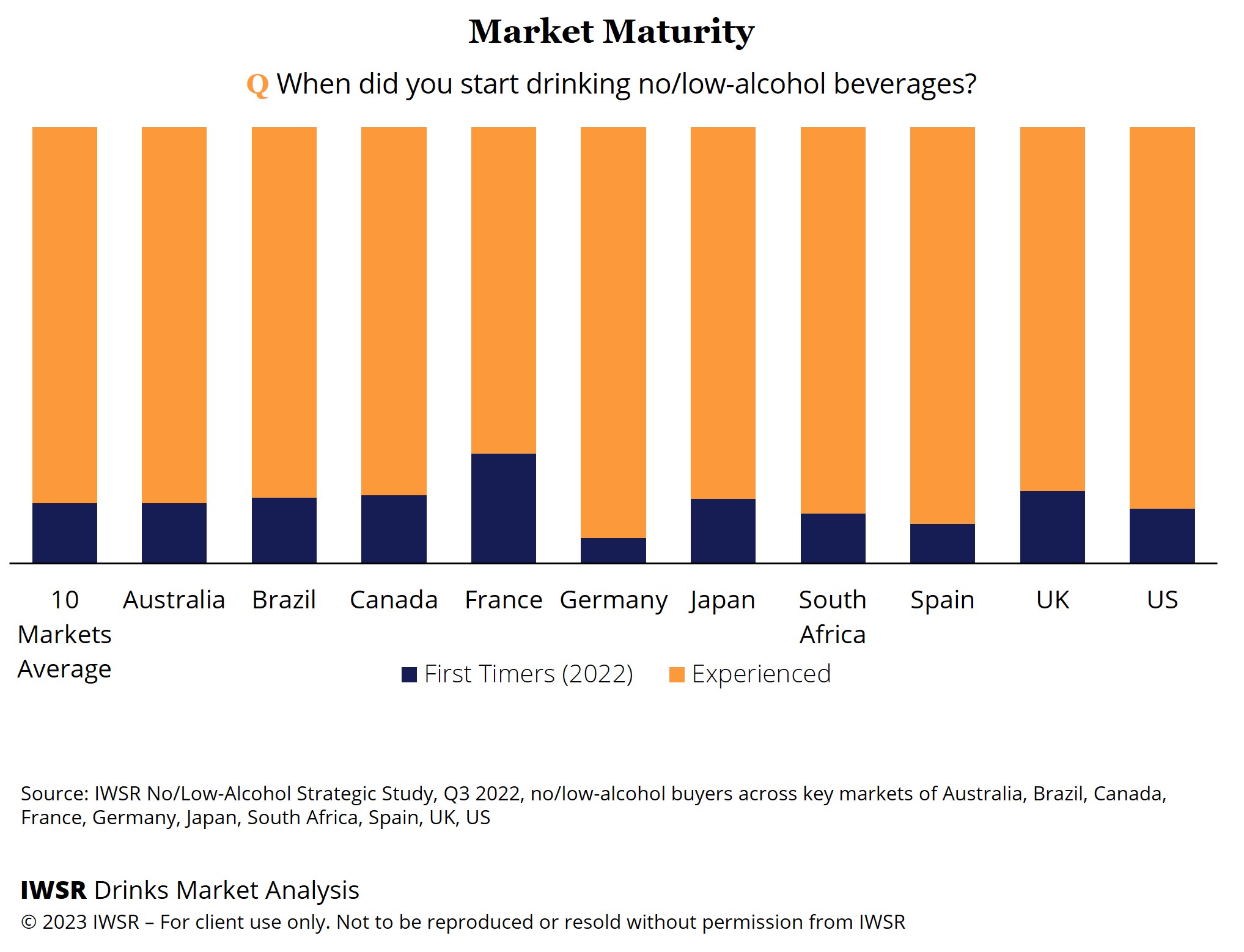

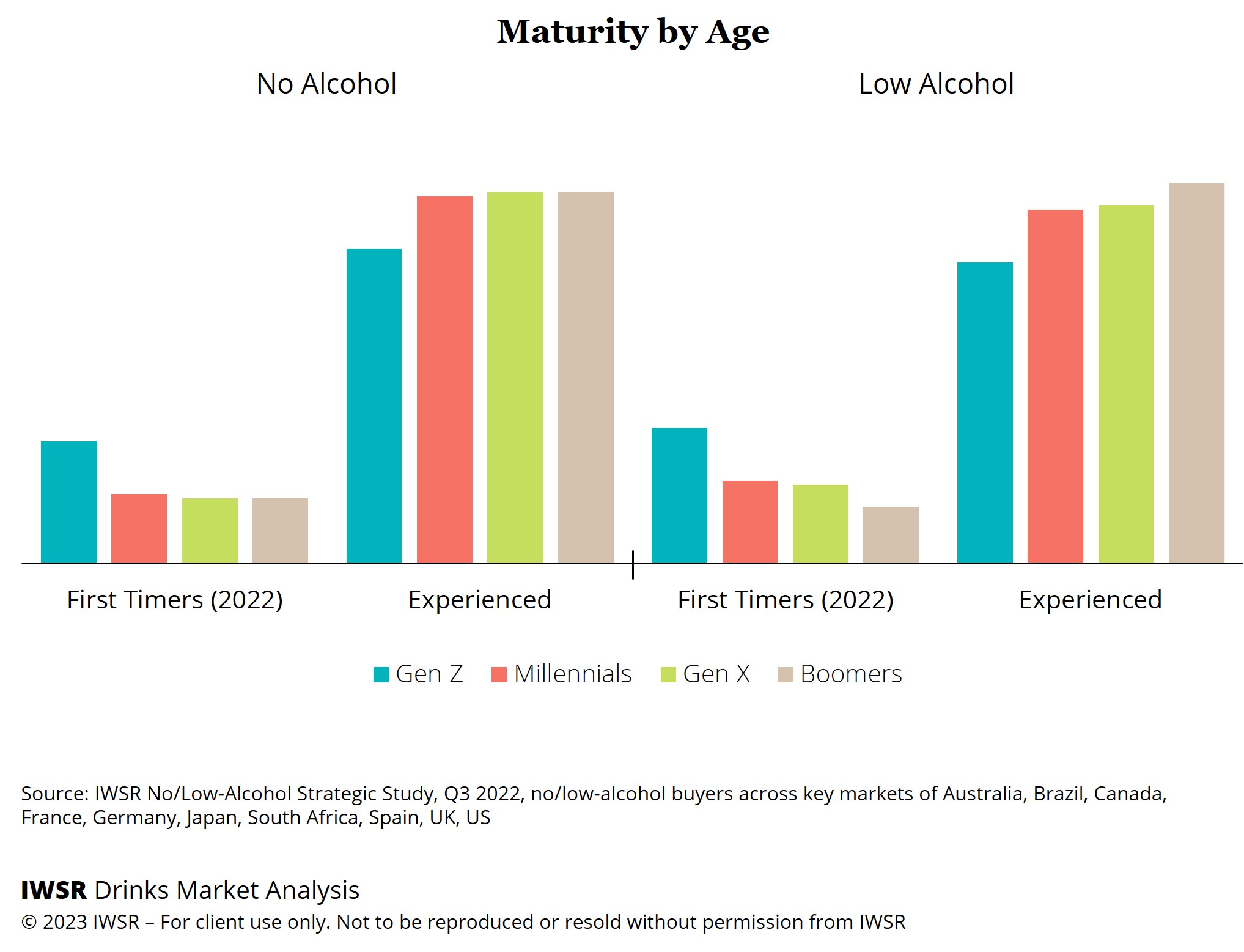

- No/low consumers are generally experienced in the category with most being consumers for more than a year; recruitment is highest in the Gen Z age group (legal-drinking aged)

- France has the highest number of new recruits, with 25% of no-alcohol drinkers joining the category in 2022.

- Germany is one of the largest no/low-alcohol markets in the world and a considerable share of older no/low consumers. This level of maturity and a lack of product innovation means that category recruitment is low, with only 6% of no-alcohol consumers joining in 2022.

- There has been a significant increase in recruits to no-alcohol in Spain.

- Australia, France and US have the highest proportion of Millennial new entrants in the low-alcohol category; and Australia, France and Canada in no-alcohol.

- 43% of US no/low consumers are Millennials, an increase on last year and by far the largest group.

- Millennials are the largest consumer group in Australia, accounting for 36% of no/low consumers. They are more likely than other age groups to be Blenders, switching between alcohol and no/low on the same occasion.

- The UK, US and Australia show the lowest proportion of Boomers for low-alcohol beverages across markets.

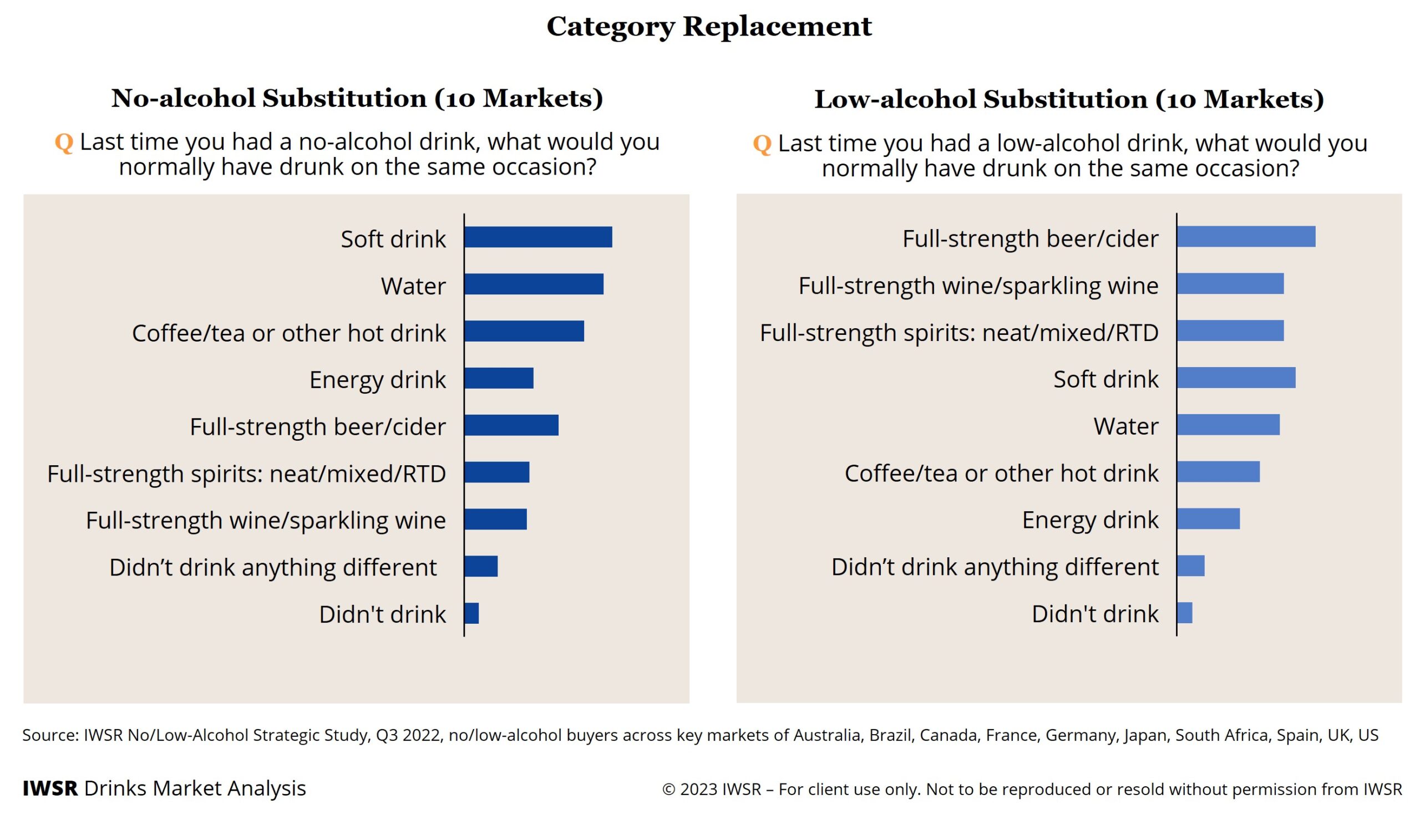

Where are consumers switching from?

- No/low consumers tend to switch between alcohol and no/low options, both in the same occasion and between different ones.

- No-alcohol is mostly replacing non-alcoholic drinks (such as soft drinks and water) in the same occasion, presenting an incremental growth opportunity for producers.

- The UK has the closest gap between replacement of alcoholic and non-alcoholic drinks, suggesting the category is more about alcohol replacement in this market than in others.

- Low-alcohol tends to substitute full-strength alcohol

- Most countries follow the same broad trend of replacing alcohol with low-alcohol.

- In the US, there is an even split between alcohol and non-alcohol being replaced with low-alcohol, suggesting that soft drinks and alcohol are swapped more than in other markets, perhaps due to a well-established RTD category and blurred category boundaries.

What’s next?

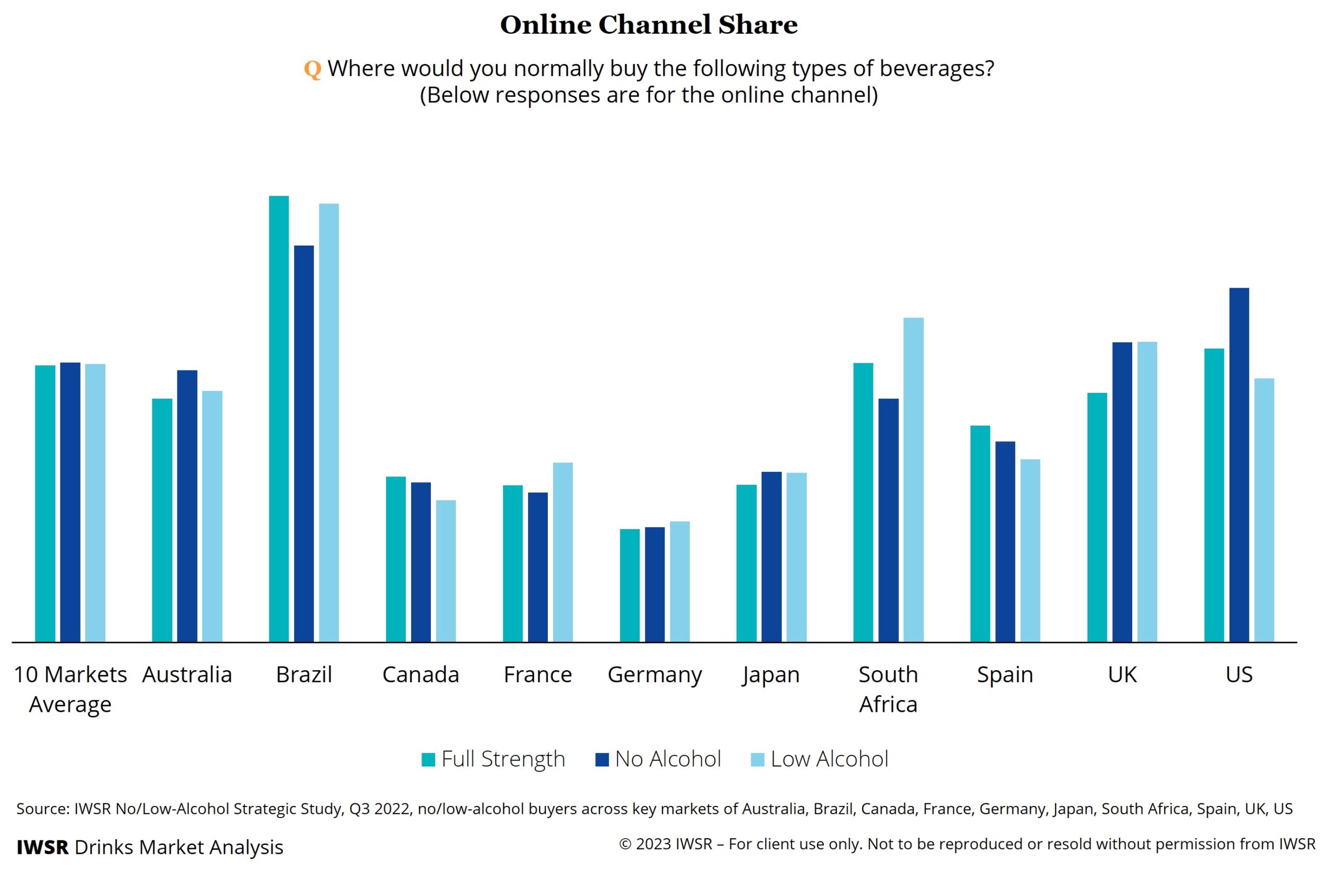

- No-alcohol is opening up different advertising and sales channel approaches than low-alcohol, with fewer restrictions bringing opportunities in ecommerce.

- Reduced restrictions on sales of no-alcohol mean it is well-positioned to take advantage of online and D2C sales, as well as to explore new outlets where people would not typically consume or purchase alcohol. Nonetheless, true integration of no/low into the consumer mindset still requires its acceptance in the mainstream on-trade, as in Spain

- Availability is a priority for further category growth. In markets like France retail shelves are still tied up by traditional no-alcohol brands that are low priced and aren’t recruiting new consumers. Shelf life of no-alcohol spirits and draught beer is a challenge.

- New markets, such as those in the Middle East; advancements in technology to help improve the taste of no/low-alcohol; product innovation; and greater recognition for no/low, are driving the outlook for the category.

You may also be interested in reading:

No- and low-alcohol category value surpasses $11bn in 2022

Key drivers for the US no/low-alcohol market

Moderation trend drives demand for no-alcohol products in the UK

The above analysis reflects IWSR data from the 2022 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All, No/Low-Alcohol | MARKET: All | TREND: All, Moderation |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies