01/07/2021

Australia and China underpin ongoing resilience for Asia Pacific beverage alcohol market

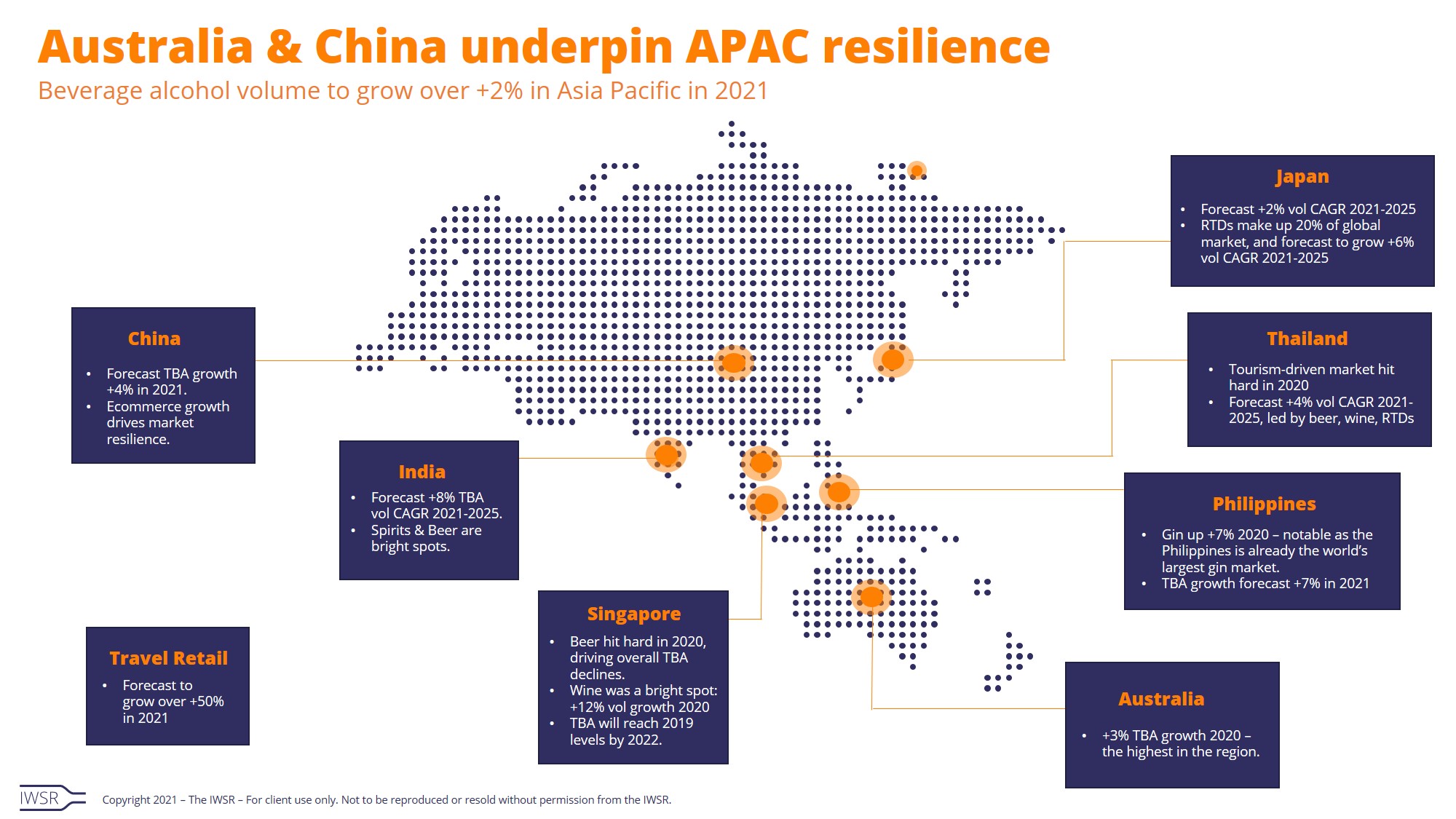

Beverage alcohol volume to grow over +2% in Asia Pacific in 2021

Beverage alcohol in Asia Pacific markets is showing positive signs of recovery, expected to gain over +2% in volume and over +4% in retail value by the end of 2021.

IWSR’s examination of 19 markets across the Asia Pacific region shows that total beverage alcohol volume in Asia Pacific decreased by approximately -8% in 2020. IWSR forecasts that long-term volume recovery in the APAC region will return to pre-Covid levels by 2025. With the exception of wine, which is expected to show volume declines at the regional level, each of the other major alcohol categories are projected to post volume growth in APAC (beer at nearly +2%; spirits under +0.5%; ready-to-drink (RTDs) at almost +6%; and cider at over +1% volume CAGR 2021-2025).

“Though an unprecedented downturn, the decline in beverage alcohol in Asia Pacific was less than previously forecast, as several factors ultimately helped the industry last year,” remarks Sarah Campbell, Research Director for Asia Pacific at IWSR Drinks Market Analysis. “The acceleration of ecommerce, growth of RTDs, strong at-home consumption in key markets, and the resilience of countries such as China and Australia, will underpin the region’s growth going forward,” Campbell adds.

Travel retail, hit particularly hard by Covid-led shutdowns in international travel and tourism, lost over -70% volume in Asia Pacific last year, but IWSR predicts volume in the channel will grow by over +50% in 2021. Green shoots in the region include the Chinese government’s decision to designate Hainan as a duty-free territory for beverage alcohol, boosting global travel retail activity long-term.

IWSR’s analysis of the beverage alcohol market in major countries in the region also shows:

Australia:

Australia is mostly an off-trade market, so growth in retail was easily able to compensate for on-premise losses in most categories during Covid, and the migration of travel retail sales to the domestic market provided an additional boost as well. In total, beverage alcohol in Australia grew by about +3% last year, the most of any country in the region. The beer category showed volume growth of nearly +3% in 2020, a bright spot against beer’s general declining trend in other global markets. The overall wine category saw a decline, but Champagne performed well, growing by more than +12%. Spirits and RTDs were the two categories that experienced the largest volume gains in 2020. IWSR forecasts that the Australian total beverage alcohol market will soften slightly over the next 5 years.

China:

The short lockdown in China, the largest alcohol market in the world, is unlikely to have long term impact on consumer behaviour in terms of beverage alcohol consumption. Due to its reliance on the on-trade, total beverage alcohol volume was hit hard by Covid (at close to -6% 2019 to 2020). However, it is expected to grow by nearly +4% in 2021. Flavoured spirits and RTDs performed well in 2020, as did single malts, which is one of the few drinks that Chinese consumers enjoy at home or in small groups (+20% in 2020). Spirits overall, however, were down close to -5% in the country last year (or close to -3% excluding national spirits, such as Baijiu). Ecommerce saw impressive growth in the market from an already large base, and online sales of beverage alcohol in China are expected to continue growing over the next five years, despite the market’s skew to the on-trade.

India:

With lockdown in India resulting in the closure of all bars and most liquor stores in the country, total beverage alcohol volume declined by close to -30% last year. The market is expected to rebound, however, to over +8% volume CAGR 2021-2025. Total spirits are forecasted to grow by almost +5% CAGR 2021-2025, and beer is expected to post growth of nearly +13% volume CAGR during that same period. Whisky in India, the dominant spirits category, was down -16% in 2020 but ultra-premium-and-above Scotch enjoyed growth, as did Irish and Japanese whiskies, driven by wealthy consumers in the market. Unlike many other countries in the region, alcohol ecommerce does not play a critical role, due to government regulations and limited channel investment.

Japan:

Total beverage alcohol was down close to -5% in Japan in 2020, but the market is expected to rebound to pre-Covid volume levels by 2024, forecasted at over +2% volume CAGR 2021-2025. The ready-to-drink category in Japan represents about 20% of the global RTD market, and grew at close to +12% in 2020. The vast majority of RTD sales in the country go through the off-trade so the category was well-insulated from lockdowns. Total beverage alcohol volume in Japan is forecasted to grow over the next five years, with RTDs projected to grow at nearly +6% volume CAGR 2021-2025.

Philippines:

Although total beverage alcohol volumes declined in the Philippines in 2020, the market is expected to post volume gains of nearly +7% in 2021, and will continue to grow over the next 5 years. IWSR forecasts that total beverage alcohol volumes in the Philippines will rebound to pre-Covid levels by 2023. Although beer volumes declined in 2020, wine and spirits volumes both increased (wine by +3% and spirits by almost +2%). Driving spirits growth was gin, up nearly +7% last year – notable given that the Philippines is already the world’s largest gin market.

Singapore:

Total beverage alcohol volume in Singapore was down close to -9% in 2020, driven by beer, which represents over 80% of all alcohol consumption in the market and saw volumes plummet due to decreases in outdoor social occasions and out-of-home dining. About 75% of wine volume in the market goes through the off-trade, which helped that category’s performance (up close to +12%) thanks to increased at-home consumption and less widespread restaurant restrictions. IWSR forecasts that total beverage alcohol volume in the country will grow by about +4% CAGR 2021-2025, bouncing back to pre-pandemic volumes by 2022.

Thailand:

The economy in Thailand was hit hard by the lack of international travel last year as alcohol sales in the country are quite reliant on Western tourists. The large local spirits market remained resilient throughout 2020 due to innovation and off-trade dominance. IWSR forecasts that total beverage alcohol will post almost +4% CAGR growth in the market 2021-2025, led by beer, wine, and RTDs.

You may also be interested in reading:

Global beverage alcohol expected to gain +3% volume in 2021

5 key trends that will shape the global beverage alcohol market in 2021

US total beverage alcohol consumption in 2020 was the largest volume gain in nearly 20 years

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All, Asia Pacific | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies