16/06/2021

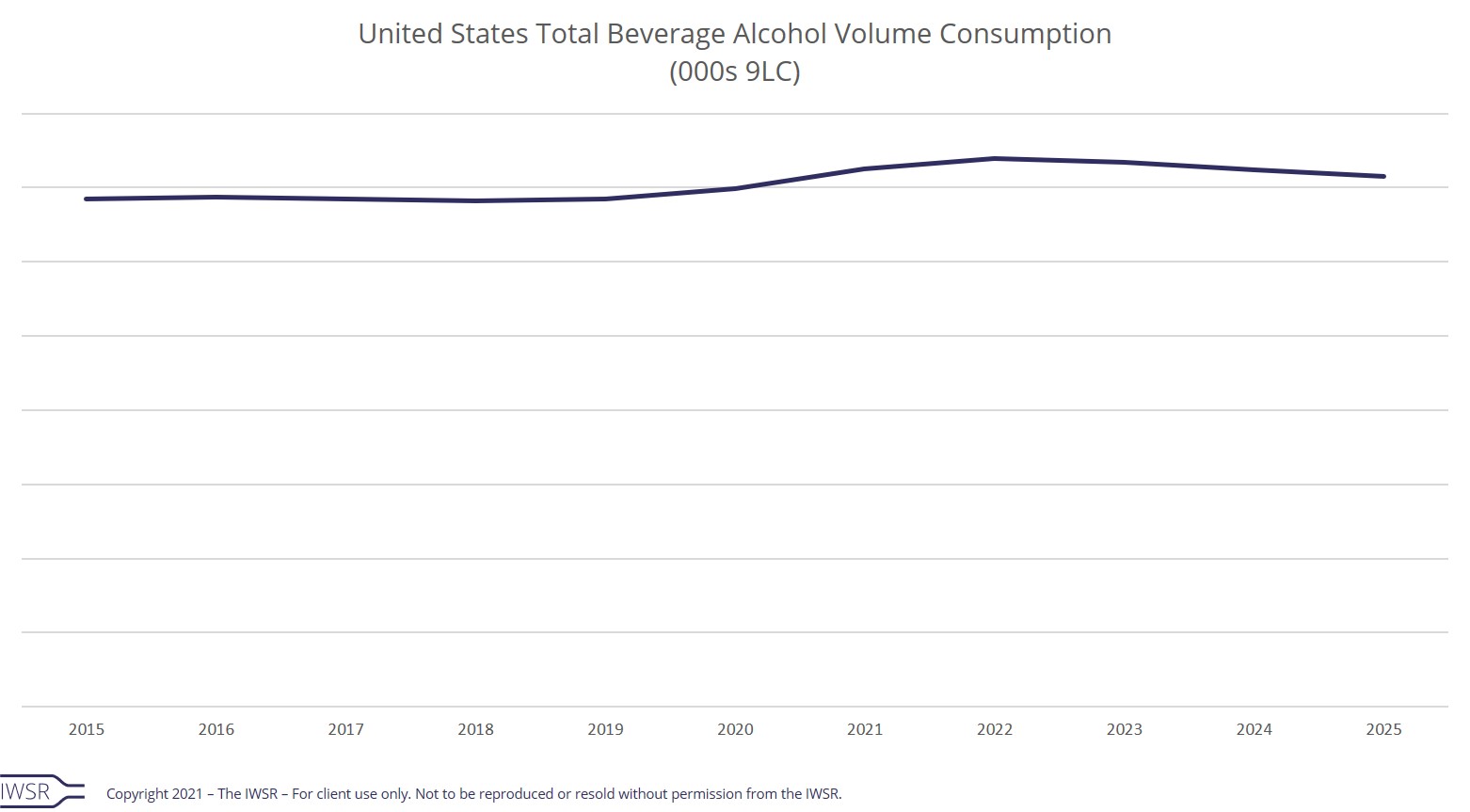

US total beverage alcohol consumption in 2020 was the largest volume gain in nearly 20 years

Driven by consumer demand for flavour, convenience, and better-for-you options, key beverage alcohol segments were accelerated by the increase in at-home occasions in 2020 in the US

Total beverage alcohol volume in the US in 2020 was up +2.0%, marking the largest gain for alcohol consumption in the country since 2002, according to new findings from IWSR. IWSR forecasts a more moderate growth rate over the next five years as normalisation returns.

“A key driver of US beverage alcohol consumption is flavour,” says Brand Rand, IWSR’s COO of the Americas. “Flavoured subcategories – from beer to vodka to US whiskey – are significantly outperforming traditional non-flavoured sub-categories. Flavour is also the top consumer driver of the fast-growing ready-to-drink (RTD) category, and that’s likely creating a halo effect on total alcohol as well.”

IWSR’s analysis of the US beverage alcohol market by category:

Spirits market in the US posts largest volume increase since 1990

In 2020, the US market posted the largest volume increase for the spirits category since 1990, with value increasing as well.

Within the category, agave-based spirits grew +15.9% in volume in 2020, overtaking rum to be the third largest spirits category in the US, behind vodka and whisky. Cognac/Armagnac was also a big winner last year and both categories are expected to continue their growth path over the next 5 years.

The whisky category showed mixed results in 2020, as tariffs negatively impacted single malt Scotch (-6.1% in volume) while bar and restaurant closures dragged down Irish whiskey. 2020 marked the first time on record that these two sub-categories post volume declines in the US. Overall, total whisky volumes grew +4.9%, led by Japanese, Indian and US whiskies, in that order. The whisky category’s growth, however, is outpacing vodka, with total whisky expected to be larger than total vodka in volume consumption by 2022.

No- and low-alcohol spirits are being driven by alcohol-free spirit alternatives and spirit-adjacent products that focus on mood-enhancing properties like adaptogens. Though trending from a small base, no-alcohol spirits are expected to end 2021 up +31.4% in the US.

Wine resonates with consumers during lockdowns

Total wine in the US grew slightly at +0.7% by volume and +1.5% by value in 2020, reversing the volume declines seen in 2019. Both still and sparkling wine volumes were up, but still wine is forecast to go back to softening declines as RTDs and spirits grow at faster rates. Despite a non-celebratory 2020, sparkling wine managed to post growth, with Prosecco (especially rosé expressions) making up for declines in Champagne consumption.

Low-alcohol wine volumes more than doubled in 2020 in the US, with major brands entering the category offering lower calorie and lower sugar options in sessionable ABVs – a direct response to RTD occasion overlap pressure. Imported wine volumes grew more than domestic US wine from markets such as Chile, Italy, and New Zealand, which did not have tariffs in place.

RTDs set to become second largest beverage alcohol category in the US, in terms of volume consumption

The biggest gains in beverage alcohol consumption in the US last year were seen across the RTD category (which includes the popular hard seltzer sub-category), making RTDs more sizable in volume than total spirits in the US, and by the end of 2021, larger than total wine.

RTDs grew +62.3% by volume in 2020, led by hard seltzers which grew +130%. Hard seltzers represent over 55% share of the total RTD category in the US, followed by flavoured alcoholic beverages (FABs), and ready-to-drink cocktails/long drinks.

“Though the cocktail/long drink sub-category is still comparatively small by volume, the segment grew +52.7% in 2020 with canned cocktail growth spurred by on-premise closures and the on-premise pivot to ‘drinks to go,’ as well as more at-home consumption and outdoor socialization,” notes Rand.

The IWSR has tracked a rise in more spirit-based RTD launches at a higher price point due to taxes in US, but volumes remain small compared to the traditional malt-based segment. However, several US states have recently passed or are reviewing legislation to reduce spirit-based RTD tax reductions.

The overall RTD category shows no signs of slowing down – IWSR expects RTDs to grow to be 22% volume share of total beverage alcohol by 2025 in the US.

No- and low-alcohol beer is a bright spot for the beer category

Beer continued annual volume declines with a -2.8% loss in the US in 2020, as volume gains in imported beer weren’t enough to sustain losses in domestic beer volume. Nonetheless, imported beer grew market share in 2020.

No- and low-alcohol beer proved a bright spot for the category, however, and the category is expected to continue to grow. Additionally, flavoured beer grew +10.4% in the US in 2020, driven by cheladas and radlers.

You may also be interested in reading:

The US and China offer resilience and opportunity for drinks groups

5 key trends that will shape the global beverage alcohol market in 2021

New technology drives ecommerce innovation in the US

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All, North America | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies