19/10/2021

RTD volume share expected to double in next five years in top markets

Ready-to-Drink products will command 8% of Total Beverage Alcohol by 2025

The market for ready-to-drink (RTD) alcohol products continues to show traction and demand from consumers. RTD volumes have been growing faster than any other major drinks category since 2018, and are expected to significantly outperform the wider beverage alcohol market over the next five years, increasing their market share to 8% by 2025 (from about 4% share in 2020) in top RTD markets.

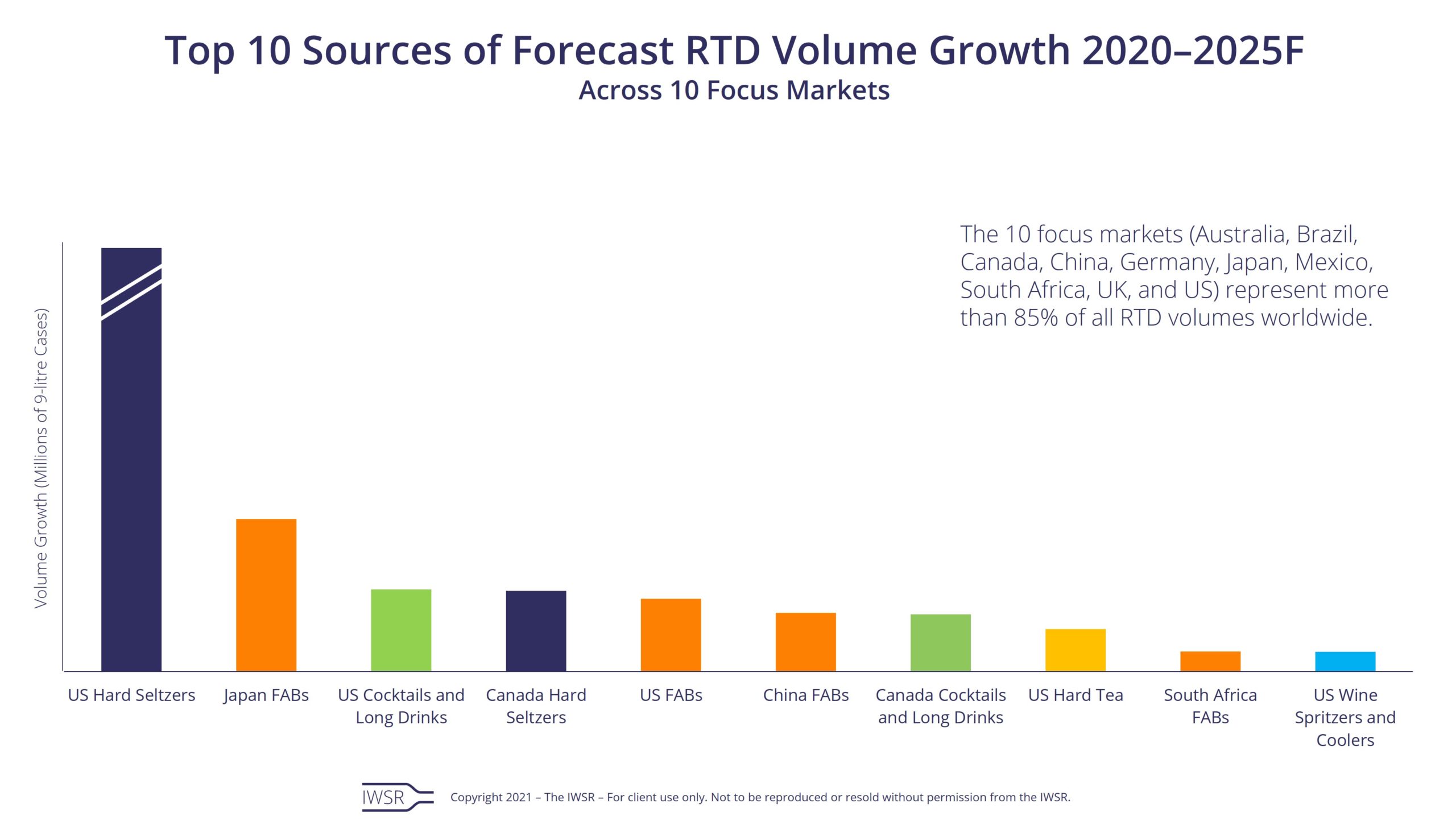

IWSR forecasts an approximate +15% compound annual growth rate from 2020 to 2025 for RTDs across 10 focus markets, compared to about +1% CAGR for total beverage alcohol during that same period. The 10 focus markets (Australia, Brazil, Canada, China, Germany, Japan, Mexico, South Africa, UK, and US) represent more than 85% of all RTD volumes worldwide.

“RTDs are still growing at higher rates than spirits, wine, and beer, signalling a major shift in consumer interest in this category across all demographics,” says Brandy Rand, COO of the Americas at IWSR Drinks Market Analysis. “But it’s important to note that RTDs aren’t only stealing share from beer, they’re also attracting spirits consumers in markets such as Australia and the UK, and cider drinkers in South Africa. We’re also seeing a significant premiumisation trend in RTDs as more and more new brands enter the space.”

Hard seltzers forecasted to remain the primary driver of RTD volumes in coming years

IWSR projects that hard seltzers will account for half of all global RTD volumes by 2025 (up from 30% share in 2020), driven by consumer demand for flavourful drinks with “better-for-you” attributes. Though much of this growth will continue to come from the US, hard seltzers are forecast to also grow rapidly in other markets such as Canada (+50% CAGR 2020-2025), the UK (+90%), China (+84%), and Australia (+24%). Across the 10 focus markets in the study, hard seltzers are expected to post total volume growth of +26% CAGR 2020-2025.

“Hard seltzer volumes outside the US are small, but awareness is also low. As that awareness grows, we’re seeing that people are increasingly willing to consider trying these products,” says Rand. “It’s important to remember that it took a few years for hard seltzers to catch on in America, and we’re still in early days in this category outside the US.”

Flavoured Alcoholic Beverages (FABs) and cocktails/long drinks drive non-hard seltzer RTD growth

In countries such as Brazil, China, Japan, and South Africa, the RTD market is driven by FABs. This sub-category is forecasted to grow by +7% CAGR 2020-2025, led by markets such as Japan, the US, and China. The other dominant RTD sub-category is cocktails/long drinks which are especially popular in countries such as Australia, Germany, Canada, and Mexico, and is projected to grow by almost +9% CAGR 2020-2025. Other rapidly growing RTD sub-categories include hard coffees, hard kombuchas, and hard teas (though from a smaller base).

Flavour is the top contributor to premium image and purchase consideration of RTDs

IWSR consumer research shows that more than half of RTD drinkers (56%) say that the regular release of new RTD flavours is the most important factor in establishing a premium image, followed by connection to a known brand (the value of brand extensions), and the use of innovative packaging. Flavour is also the key driver influencing purchase of RTDs, preferred by almost 70% of consumers. IWSR research also shows that there is a clear preference among consumers for spirit-based RTDs in most markets, as these generally have connotations of superior quality (vodka in particular is highly favoured as a base), though malt-based products are gaining share as well, driven of course by the rise of hard seltzers.

The diversity and innovation of RTDs offers opportunities for companies across the drinks market

RTDs have proven to be an effective opportunity for companies and brands from across the full spectrum of the drinks market. For example, brewers and soft drink companies have found particular opportunities in hard seltzers, becoming a major driving force behind that sub-category’s recent growth. Spirits and wine producers too have leveraged their existing brand awareness and equity to move into RTDs, from pre-mixed cocktails to hard seltzers to wine spritzes and coolers.

“It’s not just consumers who benefit from interesting and innovative RTD products, so too do global drinks companies. More than any other category, RTDs have truly captured and leveraged the trend of convergence in the beverage industry,” adds Rand. “Many well-known brands, from water to energy drinks to coffee, have recently crossed over into alcoholic RTDs, leading to a number of strategic partnerships between soft drinks, beer, and spirits companies in order to successfully leverage distribution across multiple outlets.”

IWSR defines seven sub-categories of ready-to-drink products:

- Cocktails/long drinks: drinks that reflect both well-known cocktails (Mojito, Negroni, Mule, Cosmopolitan) and common mixed drinks containing a base spirit and a non-alcoholic mixer (for example, gin and tonic or vodka and soda), where the base alcohol is clearly identified

- Hard seltzers: composed of a blend of carbonated water and alcohol, in some cases with added fruit flavour, and typically malt-based but can also be wine- or spirit-based. In contrast to long drinks, the alcohol is not defined

- Hard coffees: alcoholic drinks which can be cold brew or creamy hard coffee

- Hard teas: alcoholic tea drinks

- Hard kombuchas: made with sweetened black or green tea, fermented, and then often blended with natural juice

- Wine spritzers/coolers: drinks which mix wine with carbonated water or sodas, or fruit juices

- Flavoured Alcoholic Beverages (FABs): this subcategory covers all other RTDs, including the likes of Smirnoff Ice and Bacardi Breezers, as well as local brands

You may also be interested in reading:

Brewers turn to product diversification to secure long-term growth in the US

How has Covid-19 altered consumer attitudes in the US?

Hard seltzers are evolving, not dying

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All, RTDs | MARKET: All | TREND: All, Convenience |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies