06/07/2023

Key trends for global travel retail in 2023

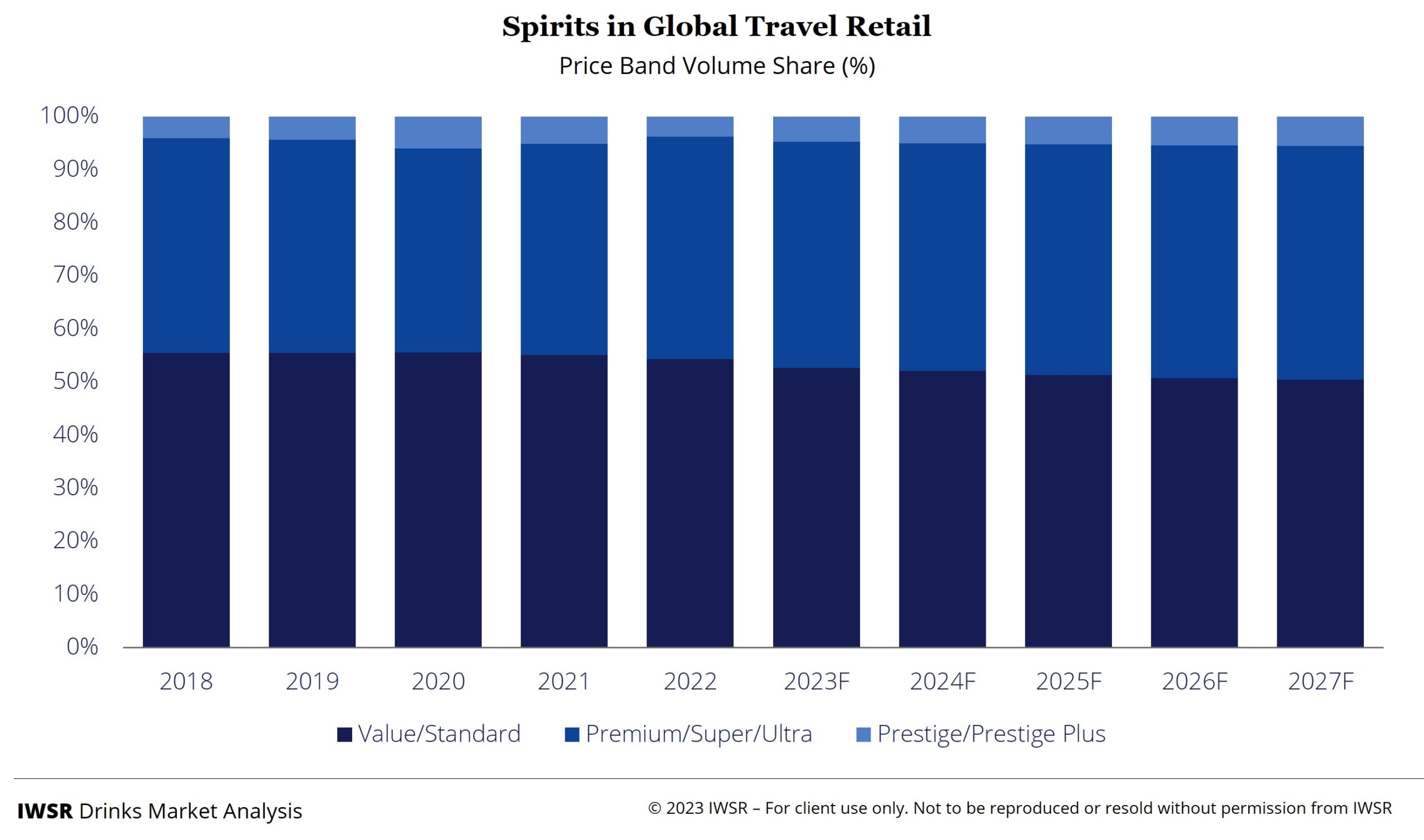

The beverage alcohol global travel retail channel is transforming, increasingly prioritising value over volume

Global travel retail (GTR) is adapting to a post-Covid world, as beverage alcohol brand owners adopt a more holistic approach and increasingly prioritise value over volume.

The pace of GTR recovery will greatly depend on the return of Chinese nationals to international air travel as pandemic restrictions ease. Champagne and whisky will spearhead GTR’s resurgence in the years ahead, but full recovery remains elusive in the short term, partly due to high global inflation and economic concerns, as well as the impact of the war in Ukraine.

The cost-of-living situation will inevitably continue to impact both business travel and tourism – in terms of expenditure, frequency and length of trips. Holidays, for example, may turn from hotel stays to self-catering, a concept that should prove beneficial for ferries, land borders and airport arrival duty free in particular. A full recovery in international air passenger numbers is now not forecast before 2025/26, according to IATA data, adding emphasis to shopper spend and basket value in order to drive revenue growth.

“The global travel retail channel is transforming as beverage alcohol brand owners reshape their strategies and adopt a more holistic approach across all global travel retail channels,” notes Emily Neill, COO Market Research, IWSR. “Brand activations will evolve to reinforce the halo effect from GTR to domestic channels. Renewed focus will fall onto sub-channels such as cruises and airline pour, and premium segments will regain market share as the channel increasingly embraces its role as a high-end product showcase.”

Key drivers for the global travel retail channel in 2023 include:

Re-imagined brand activations that target the luxury consumer

As beverage alcohol brand owners reinvest in GTR following the Covid-19 pandemic, they have seized the opportunity to change their approach, integrating GTR into a strategy spanning domestic and duty-free channels.

This greater synergy should help to maintain consistent availability of the highest-end products in GTR, which typically have restricted supply and, in the past, were often reallocated to what were seen as more profitable domestic markets.

It should also boost marketing investment in GTR, with enhanced point-of-sale materials and activations targeting the broader luxury consumer.

“The rise of standalone boutiques, shop-in-shop concepts, pop-ups and tie-ins with non-beverage luxury brands in GTR environments are all indications of brand owners seeking to target not only the high-end drinker, but also the more general luxury shopper who may also be after fashion, accessories or cosmetics,” explains Jairo Lopez Suarez, Head of Global Travel Retail Insights, IWSR.

China: international travel – and Hainan redux

The strength of the post-Covid GTR recovery will hinge on the return of international Chinese travellers to the channel. While this will be keenly felt at airport hubs in Asia-Pacific, destinations in Europe and North America will also benefit.

“GTR – not only in APAC, but around the world – is waiting a pick-up in international travel activity by Chinese nationals after pandemic rules were relaxed in early 2023,” says Suarez. “Hub airports and points of departure for flights back into China will be key – more so than Chinese airports.”

This raises questions about the future of Hainan, the duty-free enclave that did so much to offset China’s GTR slump during Covid-19. Declines recorded at Hainan in 2022 are expected to persist in 2023 as value is diverted to international GTR.

However, IWSR expects Hainan to bounce back in 2024 thanks to a resurgence in domestic traffic, but with less emphasis on the highest price segments.

“The sheer size and growth of China’s burgeoning middle class, who will be adopting Hainan as a travel destination, is believed to be fuel enough to compensate for those Chinese nationals who are now ready to rejoin the international travel circuit,” says Suarez. “There are also signs that Hainan is beginning to attract an international audience.”

Champagne and whisky key drivers for GTR

While gin has led the GTR spirits recovery, and agave spirits sales surpassed 2019 levels in 2022, the much larger whisky category will play a crucial role in the years ahead.

GTR whisky volumes grew by 77% in 2022, according to IWSR figures, and are expected to rise by 16% in 2023, recording a CAGR increase of +8% between 2023 and 2027.

“Whisky proved the key engine for volume recovery in 2022, notably US whiskies benefiting from strong performance in the Americas,” says Suarez. “Blended and malt Scotches also posted strong growth in 2022, but from a deep drop, and are still way short of pre-crisis volumes (-22% for malt, -26% for blends).”

Brandy’s recovery has been less positive – especially Cognac, hit by soft demand among US consumers and the absence of Chinese travellers, its two most important consumer groups.

But Champagne is expected to recover to pre-pandemic levels during 2023 after GTR volumes rose by 83% during 2022, according to IWSR data.

“The return of the Chinese traveller is less important for Champagne than it is for spirits – European travellers are the leading consumer group,” explains Suarez. “As Europeans are, however, particularly squeezed by inflationary pressures and the tightening of the cost-of-living situation, future growth rates of Champagne are expected to level off.”

You may also be interested in reading:

Key statistics: the no-alcohol and low-alcohol market

The 8 drivers of change for beverage alcohol in 2023 and beyond

Global beverage alcohol shows subdued growth 2022-2027, whilst value outlook is more positive

The above analysis reflects IWSR data from the 2023 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All, Travel Retail | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies