07/12/2021

Led by the US, beverage alcohol ecommerce value expected to grow +66% across key markets 2020-2025

Younger legal-drinking-age consumers drive shift from ‘traditional’ ecommerce channels to more ‘modern,’ app-led online platforms

Over the next five years, total beverage alcohol ecommerce sales across key global markets are expected to grow by +66%, to reach more than US$42 billion, according to IWSR findings.

Among 16 focus markets examined by IWSR (Australia, Brazil, Canada, China, Colombia, France, Germany, Italy, Japan, Mexico, Netherlands, Nigeria, South Africa, Spain, the United Kingdom and the United States), ecommerce value increased by about +12% in 2019, and then by almost +43% in 2020 during the height of the pandemic. Looking ahead to 2025, ecommerce is projected to represent about 6% of all off-trade beverage alcohol volumes, compared to less than 2% in 2018. The greatest forecast ecommerce value growth will come from the US, thanks to average annual growth in the country of about +20%, which will see it become the top global market for online beverage alcohol. China, which currently accounts for a third of total ecommerce value, is expected to expand less rapidly, but still contribute substantial value.

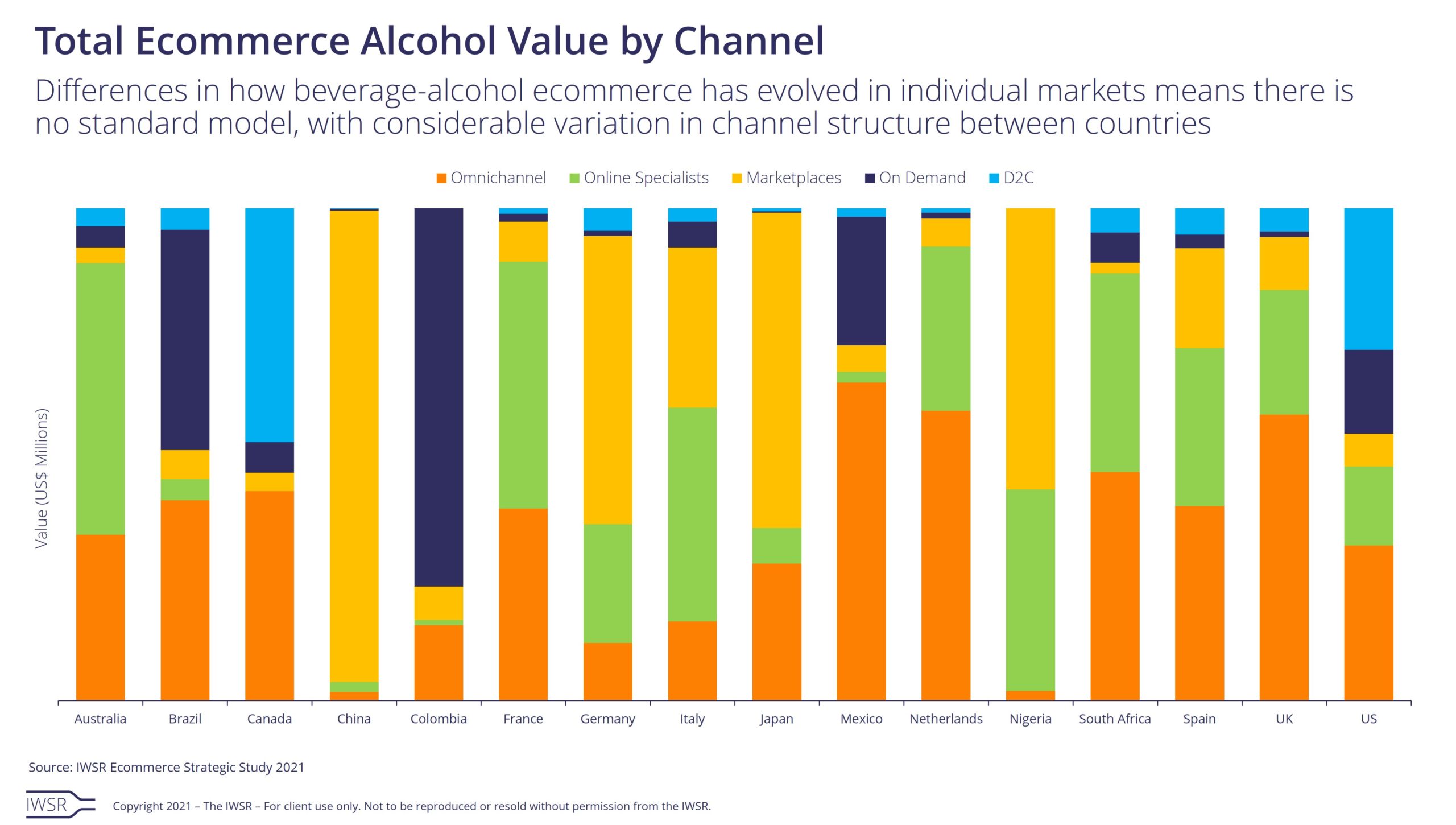

IWSR findings also show that online business models for alcohol sales are becoming more diverse, leading consumers to increasingly shift between channels and retailers according to their specific needs at any given time. In general terms, the online beverage alcohol space can be perceived as two distinct, but overlapping, worlds: more ‘traditional’ ecommerce – often omnichannel or online specialists – accessed via websites and used by older consumers seeking good prices and known brands and who are prepared to wait for delivery; and more ‘modern’ app-driven ecommerce – often on-demand or marketplaces – used by younger legal drinking age consumers willing to pay for rapid delivery and looking for interesting/premium brands.

“Given the pandemic and overall changing consumer shopping behaviour, it’s certainly not surprising that alcohol ecommerce is growing very quickly. But what’s interesting is to see the significant variations that have developed both across and within markets in how different consumer groups shop via ecommerce and what their priorities are,” says Guy Wolfe, Strategic Insights Manager, IWSR Drinks Market Analysis. “Ecommerce has clearly become engrained for many consumers, cementing its place as the third sales channel for beverage alcohol purchase.”

Consumer research conducted by IWSR found that around one-quarter of alcohol drinkers across the globe report buying alcohol online, with two-thirds having made their first purchase pre-pandemic. China has the highest proportion of online shoppers among all beverage alcohol buyers, at nearly 60%, and the US has the highest proportion of online buyers who made their first purchase during the pandemic (54%).

In most markets, wine is the largest major alcoholic drinks category in ecommerce (representing about 40% of total ecommerce value), with notable exceptions being China, Colombia, Mexico, and Nigeria, where spirits lead online sales by value. Although currently accounting for less than one-fifth of total ecommerce value, beer, cider, and RTDs are expected to grow strongly over the next five years, gaining share mainly from wine.

[table id=11 responsive=stack /]

You may also be interested in reading:

Drinks companies diversify as category lines blur

Should spirits companies adopt FMCG strategies to win in hard seltzer space?

Should brand owners buy their way into ecommerce?

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All | TREND: All, Digitalisation |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies