10/06/2021

Will the growth of ecommerce cannibalise sales or offer incremental value?

IWSR analyses the impact and opportunities of ecommerce post-Covid-19

In many global markets, Covid-19 accelerated the impact and growth of some of the industry’s key drivers, including ecommerce development, premiumisation, moderation, the rise of the so-called ‘home-premise’, and the need for more convenient product formats. These are the trends that will also underpin the industry’s resilience as it adapts to meet consumers in the years to come.

“The ability to rapidly pivot from on-premise to off-premise and ecommerce was an important factor behind many of the stronger market performances last year. The boost in ecommerce facilitated the rise and sophistication of the home-premise as well, especially in developed markets,” says Guy Wolfe, strategic insights manager, IWSR Drinks Market Analysis. IWSR data shows that the value of global ecommerce sales increased in 2020 by 45%.

Although some cannibalisation of sales from bricks-and-mortar retail and the on-premise is inevitable, ecommerce can give brand owners the opportunity to build incremental sales by focusing on higher-value, niche and limited-edition products, as well as opening up a new and valuable communication channel with consumers.

“Ecommerce has grown considerably during the [Covid-19] lockdowns, by necessity, and we have every reason to believe that this channel of distribution will remain more important than before the pandemic,” says Pierre-Yves Calloc’h, chief digital officer at Pernod Ricard.

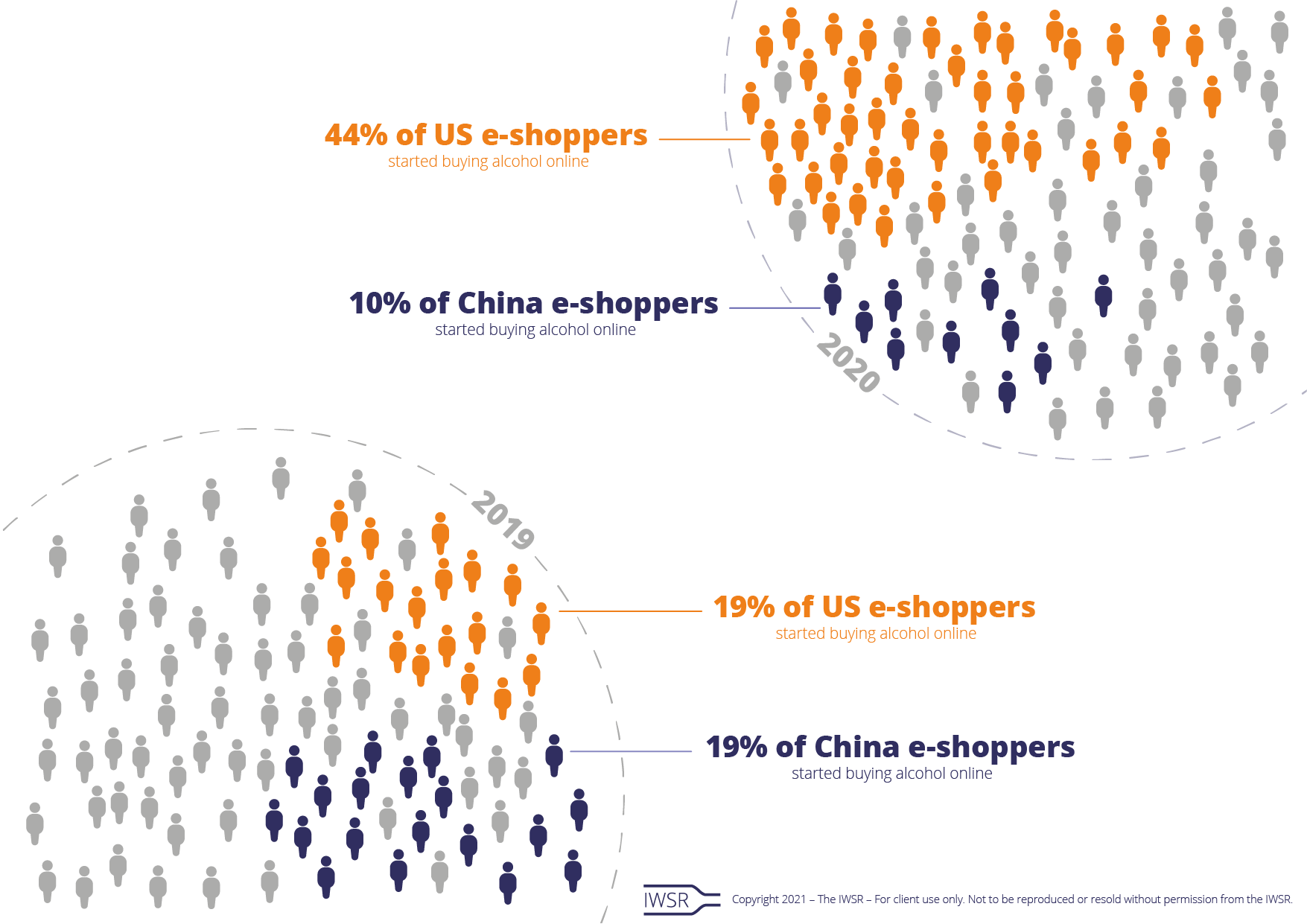

The pandemic certainly boosted consumer awareness of the possibilities of purchasing alcohol online. IWSR data shows that in markets such as the US, the pandemic accelerated the adoption rate for alcohol purchasing online: 44% of alcohol e-shoppers in the US started buying alcohol online in 2020, compared to only 19% in 2019. In mature ecommerce markets, such as China, most of the online demand is driven by older millennials. “China has a population of almost 400m millennials, so there is still room for further growth even though use of ecommerce for alcohol is well established,” notes Wolfe.

Brand owners have been swift to react, with Diageo North America more than doubling its A&P (advertising and promotional) spend in ecommerce between 2020 and H1 2021 – but is the flipside of this ecommerce surge a decline in traditional retail sales?

“A large proportion of ecommerce growth is likely to be cannibalisation,” says Wolfe. “After all, people are not necessarily going to start drinking a huge amount more overall just because of the convenience of buying online. But they may buy a bit more – and, crucially, they may also trade up in terms of product.”

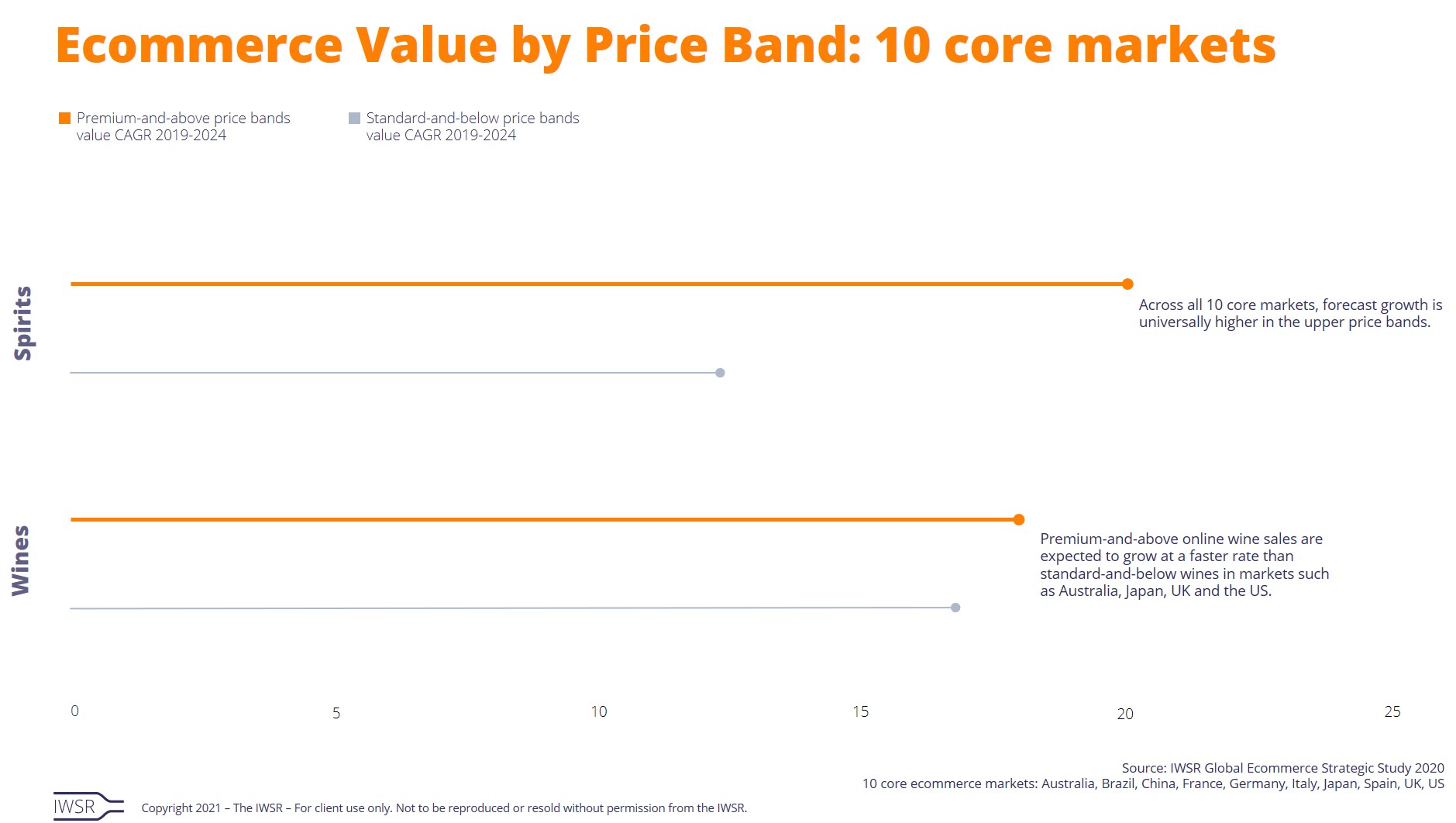

Developing this last point, Wolfe adds: “IWSR data shows that ecommerce purchases tend to be higher value [see chart below]. Often when consumers shop online, it is because they want something special, different or interesting, rather than the standard brand they buy every week. Online lends itself well to higher-value products, as retailers are able to offer a wider range without being so hampered by the limitations of physical shelf space or fast ROS [rate of sale].”

IWSR’s data is underscored by the experience of brand owners. “Our ecommerce business has a more premium mix of brands, and the rate per case is typically 15–25% higher than our business in bricks and mortar,” Diageo North America president Debra Crew told an investor call in November 2020. “Ecommerce consumers tend to be younger, more urban and very interested in discovery, which [favours] whiskeys, tequilas and higher-priced products.”

Calloc’h echoes this point: “Depending on the part of the portfolio, ecommerce will clearly provide additional sales,” he says. “This is particularly true for the luxury portfolio. Customers will not wait for premium or convenience products that they can find around the corner – but they can wait a few days to receive a very specific, high-end bottle they have ordered online.”

This aspect of consumer psychology could also benefit niche brands with a limited retail presence. “Products with limited distribution will also certainly benefit from ecommerce,” says Philippe Jouhaud, sales and marketing director for Bacardí-owned brands Noilly Prat, Bénédictine, Baron Otard and D’Ussé. “It will certainly benefit products with limited access to bricks and mortar as well as products that come as limited editions, or in special gift packs, offering an experience to consumers.

“For smaller brands, such as the brands I take care of, online retailers are definitely an opportunity for additional distribution, and therefore a way to reach new consumers.”

Consumer interest can be piqued further with channel-exclusive products. Thibaut Delrieu, sales director at Thomas Hine & Co, says: “Our sales continue to grow significantly with Amazon in the UK and Germany. We are developing an exclusive blend for them that should be available for OND [October/November/December 2021]. It will be an even more premium product than our current Hine Rare [VSOP], maybe with a new concept for Cognac.”

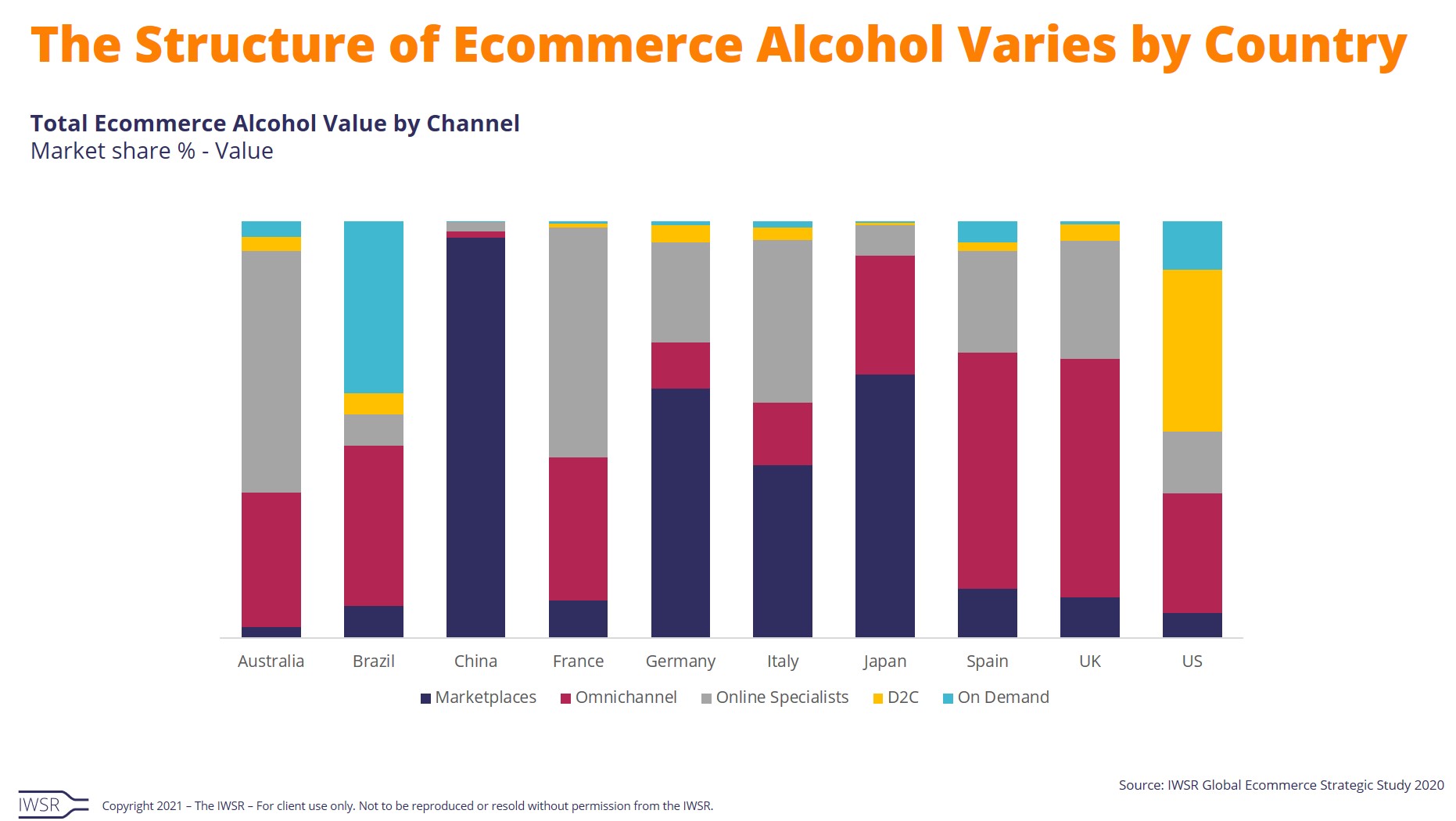

As ecommerce becomes more sophisticated around the world, the number of potential retail partners is growing – from grocery multiples with a mass-market focus to online marketplaces and online category specialists with a clear premium slant, such as The Whisky Exchange or Master of Malt. At the same time, brand owners are increasingly setting up their own direct-to-consumer (D2C) platforms and cutting out the middleman.

“Historically, most brand owners have used third parties to ‘test the water’ and start their ecommerce journey without the initial outlay of setting up their own D2C website,” explains Wolfe. “Online marketplaces can take the hassle out of the logistics, but they can be quite restrictive in terms of setting prices, for example.

“By contrast, D2C sites allow you to control everything, from the price to the relationship and conversation with the consumer. This is extremely valuable, so – spurred on by Covid-19 – brand owners are increasingly moving in this direction, including the smaller and craft players that lost their crucial on-trade channel and that could be overwhelmed by larger and better-known brands in the online marketplaces.”

In the US, new technology is helping brand owners and retailers to navigate the regulatory landscape more efficiently online. This is perhaps best illustrated by the rise of ‘white label’ storefronts, which enable brand owners to offer consumers a D2C experience while staying within the three-tier system, such as those offered by Thirstie, Bottlecapps and Speakeasy Co, to name a few. When consumers make what appears to be a D2C purchase, fulfilment of the order is passed on to retail partners, typically omnichannel players (retailers with bricks-and-mortar sales at the forefront) or online specialists.

“In the US, white-label storefronts tend to be leveraged most often by premium brands and craft offerings, compared to mainstream products with full distribution networks and/or larger budgets to spend on premium placements in third party ecommerce platforms,” remarks Adam Rogers, research director for North America at IWSR.

Larger companies tend to use a variety of approaches, combining their own D2C operations with partnerships with a number of ecommerce operations: Diageo’s virtual brand stores hosted by Amazon, for example, act as hubs for brand and category education that also convert consumer interest into physical sales.

“You have to be where the traffic is, and a brand’s website will offer more information and more experiences, with the right level of service that high-end products deserve,” says Calloc’h.

This is another potential benefit of ecommerce, and particularly of D2C platforms: consumer marketing and communication can be enhanced by conveying a wealth of brand information to purchasers and, in return, valuable consumer data and insights can be harvested.

“Beyond generating additional business, ecommerce is allowing us to communicate more with our consumers, learn more about them and their expectations, and educate them about our brands,” says Jouhaud.

[table id=10 responsive=stack /]

You may also be interested in reading:

The US and China offer resilience and opportunity for drinks groups

5 key trends that will shape the global beverage alcohol market in 2021

New technology drives ecommerce innovation in the US

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All | TREND: All, Digitalisation |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies