08/06/2022

Global beverage alcohol rebounds, with value reaching US$1.17 trillion

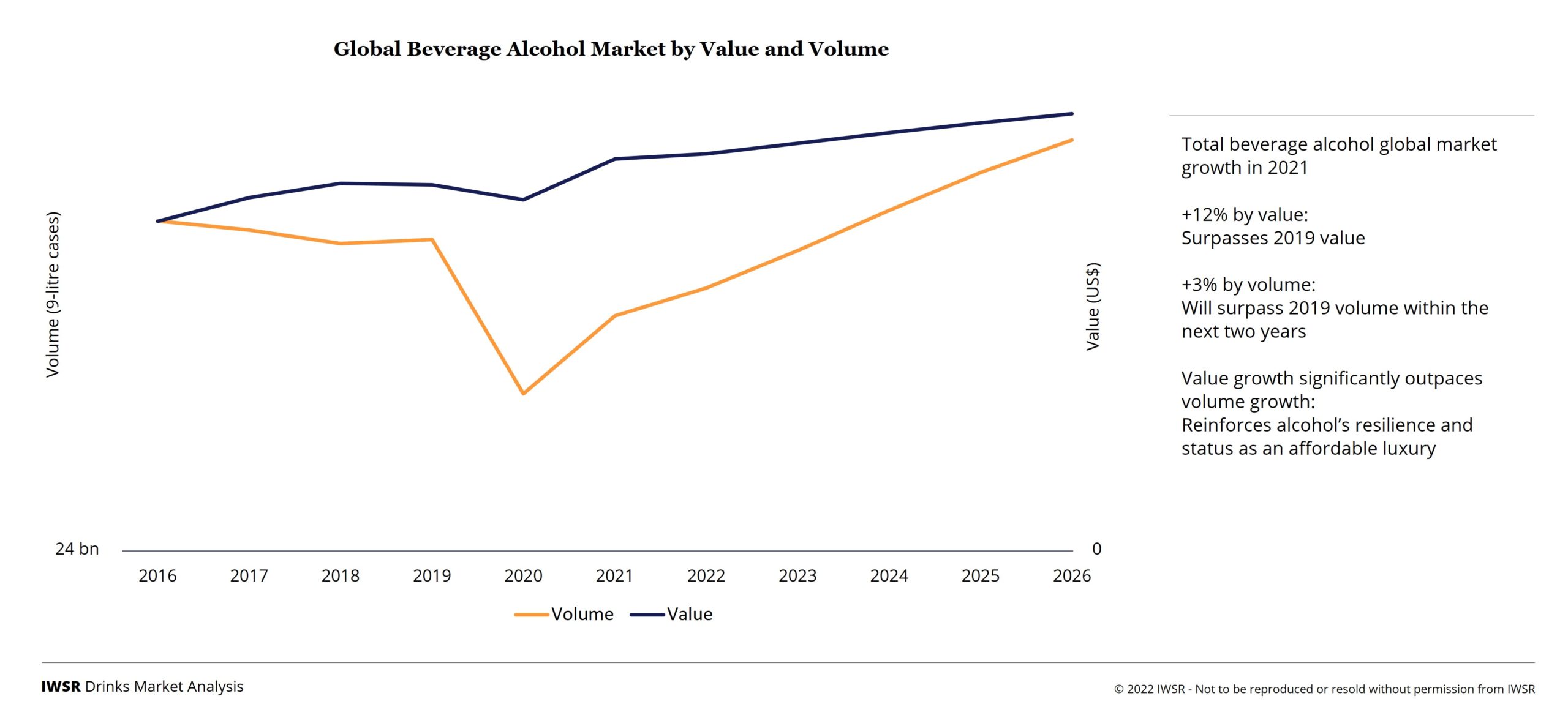

New IWSR data reinforces alcohol’s resilience and status as an affordable luxury, as value growth significantly outpaces volume growth

Global beverage alcohol value grew by +12% last year to reach US$1.17 trillion, making up for Covid-driven value losses of -4% in 2020. Total alcohol volume grew by +3% in 2021, after losses of -6% the year prior.

Examining the industry from across 160 countries throughout the world, IWSR forecasts compound annual volume growth of just above +1% for total beverage alcohol over the next five years, as Covid restrictions continue to ease.

“Our latest data shows encouraging signs for the continued recovery of beverage alcohol,” says Mark Meek, CEO at IWSR Drinks Market Analysis. “The market rebounded far more quickly than expected and, in value terms, 2021 is now above 2019. Premiumisation continues unabated; beverage alcohol ecommerce also continues to grow, although at a more moderate rate; and the trend towards moderation continues, with no/low-alcohol products seeing ongoing growth from a relatively low base. Despite the industry’s current and future challenges – ongoing supply-chain disruptions, inflation, war in Ukraine, travel retail’s slow return to pre-2019 levels, and China’s zero-Covid policy – beverage alcohol is in a strong position.”

Has the beverage alcohol market fully recovered from the pandemic?

The global beverage alcohol market is expected to surpass 2019 volumes within the next two years. While beer, cider and international spirits have not yet reached 2019 volumes, they have all met or surpassed 2019 levels in value terms. Wine has also surpassed 2019 value levels, though overall global category volumes are expected to continue on a downward trajectory.

Where are the growth markets for beer?

Beer rebounded strongly in several major markets once Covid restrictions ended, and is forecast to add significant value to total beverage alcohol over the next five years, especially in Asia-Pacific and Africa, which combined will add close to US$20 billion to the beer category by 2026. Ongoing volume growth will be seen in Brazil; the strong rebound in Mexico and Colombia that began last year will continue; and there will be some recovery in China.

What is the outlook for the spirits category?

Total spirits volume grew +3% in 2021, and value increased by +15%. This growth was driven primarily by consumers continuing to treat themselves to higher-end products, while also becoming more comfortable with making cocktails at home during pandemic lockdowns – a learned behaviour that consumers can quickly pivot to when inflation hits. IWSR forecasts that spirits volume will grow by +5% and value by +15% (2021–26).

Total whisky, which commands about a quarter of all global spirits volume (excluding national spirits such as baijiu, soju, and shochu), is expected to post volume growth of +23% and value growth of +29% over the next five years. Growth will continue in whisky’s largest global markets – India and the US. The whisky category in India will see volume growth of +23% (2021–26). In the US, by the end of this year, whisky will be bigger than vodka by volume – for the first time in almost two decades.

Global volume growth will also continue in almost all other spirits sub-categories over the next five years, including gin (+24%), Cognac (+23%) and rum (+13).

Will growth in agave-based spirits plateau?

Last year saw higher than expected growth in agave-based spirits, which is forecast to deliver significant global value increases 2021–26, at +67%. The US is the world’s most valuable market for agave-based spirits. In the UK, the category’s most valuable market in Europe, agave-based spirits are forecast to grow by more than +88% in value 2021–26, albeit from a relatively low base.

What is driving growth in the wine category?

Global still wine volumes were down -2% last year, but value was up by +5%, as the ‘less but better’ trend continues to underlie the trajectory of the still wine category. Noteworthy gains in wine were seen in the sparkling category as consumers returned to celebratory occasions in full force with the lifting of Covid restrictions. Champagne posted volume growth of +24% last year, and other sparkling wines were up +7.5%. Over the next five years, the global wine category is forecast to continue on its trajectory of long-term volume decline (-1%, 2021–26), but will see value gains of +5%.

Will premiumisation continue?

Premiumisation continues unabated for spirits and wines in the premium-and above price tier. Premium-plus spirits (priced US$22.50+) are forecast to grow by more than +50% in value in the Americas 2021–26; over +40% in Africa and the Middle East; over +20% in Europe, and just under +20% in Asia-Pacific. In fact, the single largest driver of beverage alcohol value over the next five years will be the growth of premium-and-above national spirits in Asia-Pacific. Globally, wine in the premium-and-above price band (US$10+) grew by +12% in value last year, and is forecast to increase in value by +16% 2021–26.

Buoyed by at-home consumption, how will the ready-to-drink (RTD) market evolve post-pandemic?

RTDs have been a stand-out category during the pandemic, increasing in volume by +14% in 2021 – on top of +26% growth in 2020. By volume, the category is now about a third of the size of the global spirits category, as well as the global wine category. Globally, RTD products are expected to grow by +44% in volume and +51% in value over the next five years.

Category growth will continue in the world’s largest RTD markets, the US and Japan. In Japan, the RTD category is expected to expand in volume by more than +30% over the next five years, driven particularly by flavoured alcoholic beverages (FABs). In the US, propelled by the popularity of hard seltzers, the RTD category saw continued volume growth at +15% last year; RTD value growth (+22% last year) will begin to outpace volume growth in the US, as the category matures and higher priced spirit-based RTDs gain traction in the market. At a lower growth rate than in previous years, hard seltzer volumes in the US are expected to overtake those of still wine within the next two years.

Where will we see growth in no/low-alcohol?

The no/low-alcohol category grew by over +10% last year, and will continue to grow over the next five years, albeit from a relatively low base. Notable growth last year came from the no-alcohol spirits segment in the UK: volume increased by over +80% in 2021, after tripling in size in 2020. Looking forward, no-alcohol beer will add the most volume to the global no/low segment over the next five years.

What consumer trends are driving future consumption?

Millennials led the global consumption bounce-back last year, being the generation least affected by the pandemic’s restrictions; these consumers (now aged 25–40) are more adventurous than older generations, and with their significant spending power and focus on ‘less but better,’ they tend to purchase more premium products. Millennials, and in some cases Gen Zs, are amongst the highest spenders on wine in markets such as Australia, Sweden, the US, and the UK. It remains to been seen if this trend continues, with governments withdrawing Covid support packages and a probable increase in unemployment rates in many markets.

The underlying consumer trends that continue to provide tailwinds for the global beverage alcohol market include: ‘better for me’ consumer drivers, such as moderation, ingredient quality and functional benefits; ‘better for the world’ values, including sustainability and social equality; and online interaction, both via ecommerce and social media, as well as new ways to engage through NFTs and the metaverse. Global alcohol ecommerce continued to grow last year (+16% in value 2020–2021), although this was at a slower rate than in 2020 (+45% in value 2019–2020).

“Challenges remain, including whether bars and restaurants will continue to attract consumers who have grown comfortable with ecommerce and at-home consumption; whether consumers will accept price increases on their preferred brands; and whether inflation and supply-chain issues will lead to consumers down-trading and gravitating towards local rather than imported products,” adds Meek. “We’re living in an age of uncertainty, and these are uncharted waters for the industry. However, as we have seen in previous crises, this is a very resilient industry sector.”

Note: All value growth figures in this article are given at variable currency rates. At constant currency, the value growth rates show that global beverage alcohol value grew by +9% last year to reach about US$1.17 trillion, making up for Covid-impacted value losses of -2% in 2020.

You may also be interested in reading:

Beverage alcohol ecommerce value expected to grow +66% across key markets 2020-2025

Key trends driving the global beverage alcohol drinks industry in 2022

No- and low-alcohol in key global markets reaches almost US$10 billion in value

The above analysis reflects IWSR data from the 2022 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies