16/12/2021

Key Trends Driving the Global Beverage Alcohol Industry in 2022

IWSR analyses the key drivers that will shape the global market landscape in 2022

Beverage alcohol has proven itself to be one of the most crisis-proof consumer goods categories at a time of significant disruption.

While government schemes and grants have kept spending buoyant in some markets, economies have been set back by disruptions to key industries. Shipment costs and delays, container shortages, higher packaging costs and rising energy costs continue to challenge the market. Meanwhile, soaring inflation and a changing political landscape have contributed to recruitment challenges in the hospitality sector. In the US, for example, inflation hit its highest level in 40 years in November 2021, up 6.8%, while the UK’s supply chain and recruitment struggles continue to be impacted by the fall-out from Brexit.

Nevertheless, consumers are increasingly comfortable with returning to the on-trade, especially the millennial and Gen X cohorts. Ecommerce has developed into a sophisticated and nuanced channel, and digital engagement has become a crucial part of the customer journey. As ecommerce and the on-premise grow in strength, structural long-term changes to the off-trade B&M will present a very different beverage alcohol market landscape in the years to come.

Here are the key trends driving the beverage alcohol market landscape, as consumer behaviours continue to shift and guide market strategies and product innovation.

Emergence of non-traditional luxury categories

Although international status spirits (spirits sold at US$100 and above, excluding Baijiu) suffered declines in 2020 at a rate that exceeded that of the total global spirits market, IWSR expects a bullish rebound in line with previous growth levels of 2014-2019.

Future category growth will be underpinned by increasing levels of wealth and new market entrants – especially in Asia and the US. IWSR consumer research, for example, shows that 39% of urban affluent Chinese alcohol drinkers said they had spent over RMB 500 (approx. US$79) on a bottle of alcohol to drink at home in the first half of 2021.

As new consumers enter the market, a key disrupter to the current international status spirits landscape is segment diversification and the emergence of niche status categories – such as agave-based spirits, Irish whiskey, US whiskey and Japanese whisky, which all registered absolute growth in 2020.

Substituters vs Blenders: moderation choices are driven by consumption occasion

No- and low-alcohol products are becoming more approachable for consumers as they are increasingly accepted as a lifestyle and societal norm. Channels solely dedicated to selling alcohol-free drinks for adult occasions are also on the rise, with dedicated ecommerce sites, retailers and bars coming to market.

A distinction in how and when consumers choose no- versus low- products is becoming increasingly evident. Across key markets, the majority of no/low consumers can be identified as ‘Substituters’ – those who use no- and low-products in place of full strength for certain occasions.

IWSR consumer research shows that in the UK, for example, 40% of no/low consumers are ‘Substituters’, with LDA Gen Z and millennials (46% and 41% respectively) more likely to substitute than Boomers (36%). LDA Gen Z and millennials in the UK are also more likely to be ‘Blenders’ where they switch between no/low and full-strength on the same occasion (20% and 23% respectively). A similar trend can also be seen in other markets, such as the US.

Tapping into no-alcohol occasions, new technologies are also enabling producers to launch alcohol-free products that offer mood-enhancing or functional benefits, many with ingredients such as CBD, nootropics and adaptogens. These products focus on how ingredients will make consumers feel, and are seen as an alternative way to enjoy traditional alcohol occasions – tapping into health conscious (and stressed out) consumers.

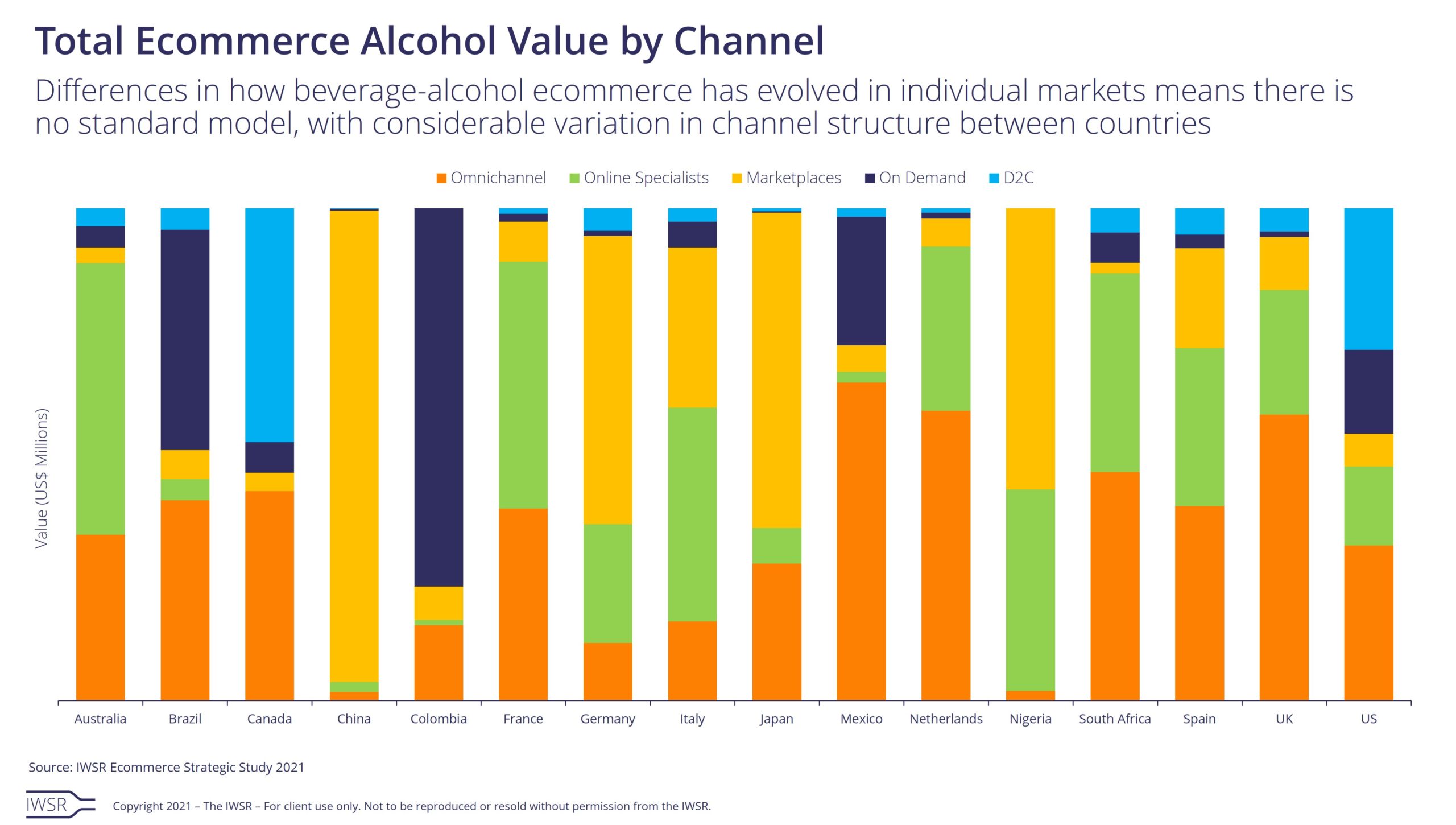

Ecommerce landscape becomes more nuanced as sub-channels blur

The value of ecommerce increased by almost +43% in 2020 across 16 key markets, up from +12% in 2019. IWSR data shows that by 2025, in these markets ecommerce is projected to represent about 6% of all off-trade beverage alcohol volumes, compared to less than 2% in 2018.

As ecommerce alcoholic-drinks sales develop, the number of retailers is increasing and the range of business models they employ is becoming more diverse and nuanced. Distinctions between different ecommerce channels, and even between online vs offline purchasing, are becoming increasingly irrelevant to consumers.

This is leading to a blurring of lines between online sales channels – for example, omnichannel retailers are establishing logistics partnerships with on-demand services in order to offer faster delivery; on-demand platforms are using ‘dark stores’ to improve delivery times and so become more like marketplaces; and marketplaces are establishing networks of physical stores.

A more sophisticated home-premise impacts the return of the on-premise

Changes in living location, work commutes and hybrid working policies mean that consumers are spending more time at-home and in local on-premise venues. As such, IWSR findings indicate that premium consumption may potentially shift, to some extent, from the on-trade to the home-premise.

As consumers return to the on-trade, their experiences will be shaped by the last two years of premium at-home experiences, such as at-home cocktail-making and subscription services. Consumers will therefore be more conscious of higher prices and more easily deterred by poorer quality products or experiences in bars, pubs and restaurants.

IWSR expects brand owners to be more selective in where they support their brands in the on-premise, likely increasing focus on the top-end and most active on-trade accounts.

Early signs of premiumisation in RTD category

New RTD launches coming to market have a higher representation of premium-and-above products than volumes consumed in 2020, suggesting a trend towards premiumisation. This marks a clear diversion from RTD innovation so far, with the vast majority of the global RTD category currently sitting within the standard-and-below price bands.

The move towards premiumisation will appeal to spirits and wine brand owners, as most of the value growth within the broader spirits and wine categories over the past decade has come from the premium-and-above segment.

While flavour is the primary purchase driver for RTD selection by consumers in key markets, alcohol base (as well as cocktail type) are also significant motivating factors, with consumers more likely to perceive spirits-based products as being of higher quality.

Spirits-based RTDs already dominate the category in most key markets – apart from in Mexico, and, most notably, in the US, where malt-based RTDs dominate. Although spirits-based RTDs hold a minority share in the US, their small volumes are driving the development of a super-premium segment – the first to be seen across the global RTD landscape.

Diversification as category lines blur

People are switching with increasing frequency between beverage options or trialling completely new beverages. IWSR research shows a wide repertoire of product trial, with consumers showing strong interest in trying craft beer, hard seltzers, wine and Japanese whisky.

Drinks companies are responding by moving into previously unexplored categories to diversify their portfolios and in some cases, proactively plan for the softening or decline of existing core brands and/or categories. Diversification also better positions beverage alcohol categories to address changing consumer tastes and the blurring of lines between traditional soft drinks and alcohol, or alcohol adjacent products, such as CBD and other enhancements.

Companies are no longer selling products to groups of consumers, but are selling products that fit particular consumption occasions. Having a wider portfolio allows them to be more exhaustive in their approach, better understand the adjacent and competing categories, and use small-scale investments to learn more about new products and occasions.

Clear commitments to sustainable practices

Sustainable packaging solutions have been at the top of corporate and social responsibility agendas in the drinks industry for many years. But concerns around climate change have been growing in intensity, especially following events such as COP26. Influential figures across the industry, as well as consumers, are increasingly looking for drinks companies to show a clear commitment to sustainable practices.

Solidarity with local brands and businesses has also been a key trend during the pandemic, and is one that is closely associated with consumers’ sustainable mindset. For example, consumer research from IWSR shows that 48% of US alcohol drinkers say their purchase decisions are positively influenced by a company’s sustainability or environmental initiatives; rising to 72% among Brazilian alcohol drinkers, and 70% of urban affluent Chinese alcohol drinkers.

Shaky international supply chains and relative price were not the only drivers of this trend: in many cases, consumers reported they also wanted to ‘do their bit’ for the local economy. Building on this crisis response, local brands may hope to reinforce their status for the long term by emphasising sustainability, quality and community values.

External pressures

Factors beyond consumer demand continue to impact production and route-to-market for the global beverage alcohol industry. Rising packaging costs, container capacity and other supply chain issues, inflationary pressures, and environmental change will impact some suppliers significantly. Some companies may therefore need to be more tactical and adjust some of their near-term market and brand strategies to adapt to the economic and operating environment.

Brand owners should also be conscious of false positives witnessed through 2020 and 2021 that will revert to previous historical trends, especially as international travel resumes. Particularly for premium beverage alcohol, the past two years saw a marked shift in where products were purchased – a trend that may reverse as the market normalises. As such, purchasing spikes seen in domestic markets throughout 2020 and 2021 will likely face some downwards correction going forward.

[table id=11 responsive=stack /]

You may also be interested in reading:

Drinks companies diversify as category lines blur

Should spirits companies adopt FMCG strategies to win in hard seltzer space?

Led by the US, beverage alcohol ecommerce value expected to grow +66% across key markets 2020-2025

The above analysis reflects IWSR data from the 2021 data release. For more in-depth data and current analysis, please get in touch.

CATEGORY: All | MARKET: All | TREND: All |

Interested?

If you’re interested in learning more about our products or solutions, feel free to contact us and a member of our team will get in touch with you.

Sign up to our newsletter

Access complimentary insights and analysis

to help you stay competitive and innovative

Head office

IWSR,

LABS House,

Floor 6, 15-19 Bloomsbury Way,

London, WC1A 2TH,

United Kingdom

Quick links

Policies